Managing cash flow is one of the most important responsibilities of any business. While companies focus heavily on increasing sales and collecting payments from customers, managing outgoing payments is equally critical. This is where the Accounts Payable (AP) process plays a vital role.

Accounts Payable refers to the money a business owes to suppliers, vendors, contractors, and service providers for goods or services purchased on credit. An efficient accounts payable process helps businesses maintain healthy supplier relationships, avoid late payment penalties, improve cash flow management, and ensure accurate financial reporting.

Whether you are a small business owner, accountant, finance professional, or entrepreneur, understanding the accounts payable process is essential for maintaining strong financial controls and ensuring smooth business operations.

In this comprehensive guide, we will explain the accounts payable process step by step, discuss its importance, examine the documents involved, identify common challenges, and provide practical examples to help you understand how accounts payable works in real-world business scenarios.

What is Accounts Payable?

Accounts Payable (AP) is a current liability that represents money owed by a business to external parties for purchases made on credit.

When a company purchases goods or services and does not pay immediately, the amount due is recorded under accounts payable until payment is made.

Examples of Accounts Payable

A business may owe money for:

- Raw materials purchased from suppliers

- Office rent

- Utility bills

- Professional services

- Software subscriptions

- Equipment purchases

- Marketing services

- Transportation charges

For example, suppose ABC Manufacturing purchases raw materials worth ₹1,00,000 from XYZ Suppliers on 30-day credit terms. Until the payment is made, ₹1,00,000 will appear as Accounts Payable in ABC Manufacturing’s balance sheet.

Why is the Accounts Payable Process Important?

An effective accounts payable process benefits businesses in several ways.

1. Improves Cash Flow Management

Proper scheduling of payments helps businesses optimize cash flow and maintain sufficient working capital.

2. Prevents Late Payment Penalties

Timely invoice processing ensures vendors are paid within agreed terms, preventing additional charges.

3. Strengthens Vendor Relationships

Suppliers prefer working with businesses that pay invoices accurately and on time.

4. Enhances Financial Accuracy

Accounts payable records contribute directly to financial statements and management reports.

5. Reduces Fraud Risks

A structured approval workflow helps prevent duplicate payments, unauthorized purchases, and fraudulent transactions.

6. Supports Regulatory Compliance

Maintaining proper records helps businesses comply with tax regulations, audits, and statutory reporting requirements.

Key Documents Used in the Accounts Payable Process

Several documents are involved throughout the accounts payable cycle.

Purchase Requisition (PR)

An internal document requesting approval to purchase goods or services.

The production department requests the purchase of 500 units of raw material.

Purchase Order (PO)

A formal document issued to the supplier specifying quantities, prices, delivery terms, and payment conditions.

Purchase Order Number: PO-2026-001

Supplier: XYZ Suppliers

Quantity: 500 Units

Price: ₹200 per Unit

Total Value: ₹1,00,000

Goods Receipt Note (GRN)

Prepared when goods are received and inspected.

Received Quantity: 500 Units

Condition: Accepted

Date Received: 10 June 2026

Supplier Invoice

A bill sent by the supplier requesting payment.

Invoice Number: INV-4567

Amount: ₹1,00,000

Payment Terms: Net 30 Days

Payment Voucher

An internal document authorizing payment.

Payment Method: Bank Transfer

Approved By: Finance Manager

Amount: ₹1,00,000

Step-by-Step Accounts Payable Process

The accounts payable process consists of several stages designed to ensure accuracy and control.

Step 1: Identifying the Need for Purchase

The process begins when a department identifies a requirement for goods or services.

For example, the production department notices that raw material inventory is running low and submits a request for replenishment.

The request typically includes:

- Item description

- Quantity required

- Purpose of purchase

- Expected delivery date

Management reviews the request before approving further action.

Step 2: Creating and Approving a Purchase Requisition

A purchase requisition is prepared and submitted for approval.

The purpose of approval is to verify:

- Business necessity

- Budget availability

- Procurement policy compliance

Department: Production

Requested Item: Steel Sheets

Quantity: 500 Units

Estimated Cost: ₹1,00,000

Status: Approved

Once approved, the procurement team proceeds with vendor selection.

Step 3: Issuing a Purchase Order

After selecting a supplier, the company issues a purchase order.

The purchase order acts as a legally binding document outlining purchase details.

- Supplier name

- Purchase order number

- Quantity

- Unit price

- Delivery terms

- Payment terms

- Delivery location

Purchase Order No: PO-2026-001

Vendor: XYZ Suppliers

Quantity: 500 Units

Rate: ₹200 Per Unit

Total Amount: ₹1,00,000

Payment Terms: 30 Days

Step 4: Receiving Goods or Services

The supplier delivers goods or completes services according to the purchase order.

The receiving department verifies:

- Quantity received

- Product quality

- Compliance with specifications

- Damage or shortages

A Goods Receipt Note (GRN) is then generated.

Ordered Quantity: 500 Units

Received Quantity: 500 Units

Condition: Good

GRN Number: GRN-2026-115

The GRN serves as proof that goods were received.

Step 5: Receiving Supplier Invoice

Once goods are delivered, the supplier sends an invoice.

The invoice contains:

- Invoice number

- Invoice date

- Purchase order reference

- Product details

- Tax information

- Payment due date

Invoice Amount: ₹1,00,000

GST: ₹18,000

Total Invoice Value: ₹1,18,000

Due Date: 30 Days from Invoice Date

The accounts payable team records the invoice and prepares it for verification.

Step 6: Invoice Verification and Three-Way Matching

One of the most important controls in the AP process is the Three-Way Match.

The accounts payable team compares:

- Purchase Order

- Goods Receipt Note

- Supplier Invoice

Payment proceeds only if all three documents match.

| Document | Amount |

| Purchase Order | ₹1,00,000 |

| Goods Received | 500 Units |

| Supplier Invoice | ₹1,00,000 |

Result: Match Successful

Payment Approved

If discrepancies exist, the invoice is placed on hold until resolved.

Step 7: Recording the Liability

After verification, the invoice is entered into the accounting system.

Purchases A/c Dr ₹1,00,000

Input GST A/c Dr ₹18,000

To Accounts Payable A/c ₹1,18,000

This entry records the obligation to pay the supplier.

Step 8: Approval Workflow

Before payment, authorized personnel review the invoice.

Approval levels may depend on invoice value.

Up to ₹50,000 – Department Head

₹50,001 to ₹5,00,000 – Finance Manager

Above ₹5,00,000 – CFO Approval

This step ensures financial control and prevents unauthorized payments.

Step 9: Scheduling Payment

Approved invoices are scheduled according to payment terms.

Common payment terms include:

- Net 15

- Net 30

- Net 60

- Advance Payment

- Partial Payment

Invoice Date: 1 June

Terms: Net 30

Payment Date Scheduled: 1 July

Proper scheduling helps optimize working capital.

Step 10: Making Payment

Payments may be made through:

- Bank Transfer

- NEFT

- RTGS

- UPI

- Cheque

- Online Payment Gateway

Vendor: XYZ Suppliers

Amount Paid: ₹1,18,000

Payment Date: 1 July

Mode: Bank Transfer

Transaction Reference: TXN458965

The accounts payable balance is cleared after payment.

Step 11: Recording Payment

The accounting entry for payment is:

Accounts Payable A/c Dr ₹1,18,000

To Bank A/c ₹1,18,000

This removes the liability from the books.

Complete Accounts Payable Process Example

Let’s see the entire process in action.

ABC Manufacturing purchases steel sheets from XYZ Suppliers.

Purchase Value: ₹1,00,000

GST: ₹18,000

Total Invoice: ₹1,18,000

Credit Terms: 30 Days

The production team requests material.

Management approves the purchase.

The procurement team issues a purchase order.

The supplier delivers the material.

The warehouse verifies receipt and creates a GRN.

The supplier sends an invoice.

Accounts payable performs a three-way match.

The invoice is approved.

Payment is scheduled.

After 30 days, ₹1,18,000 is transferred to the supplier.

The AP account is closed.

The transaction is successfully completed.

Common Challenges in Accounts Payable

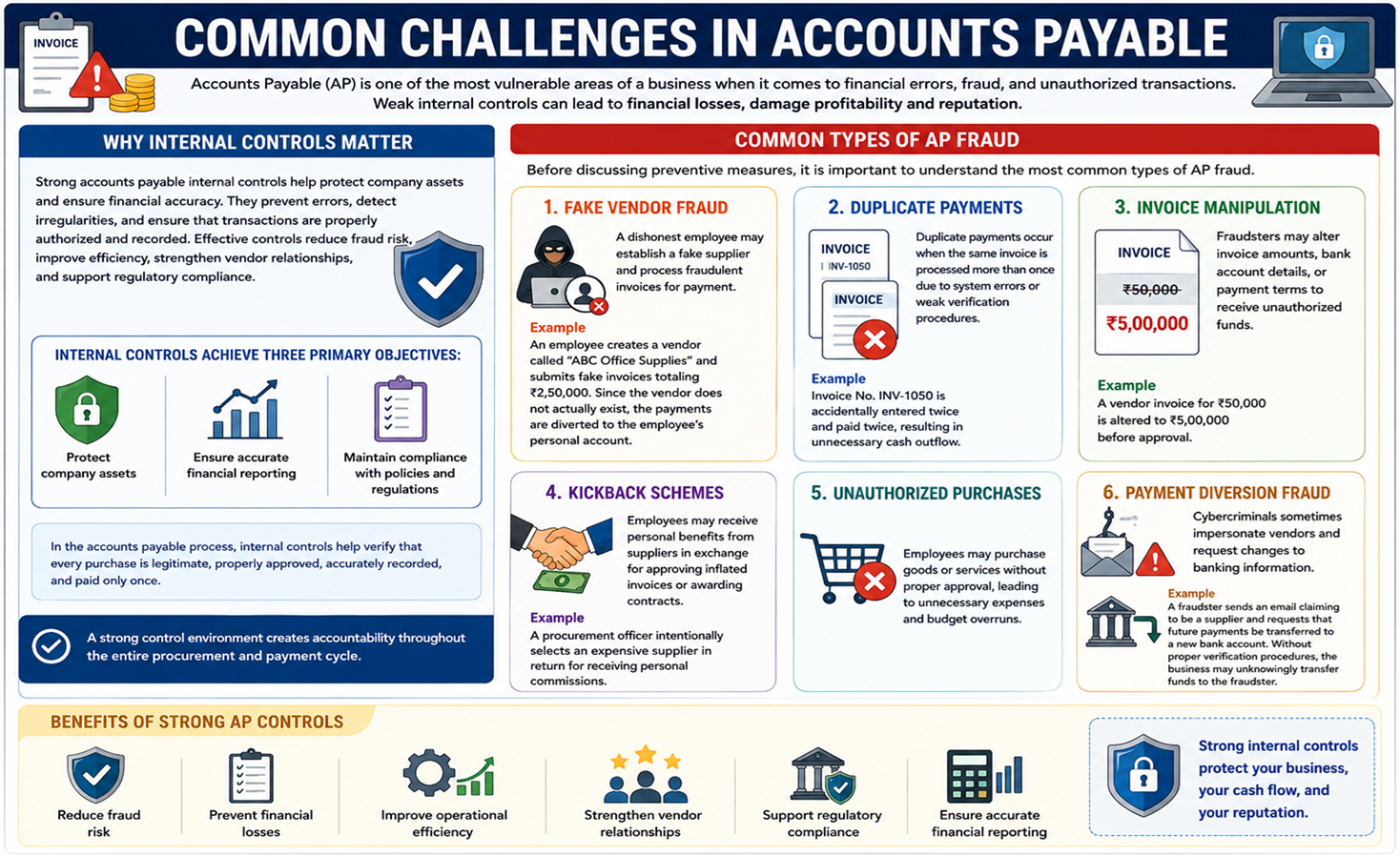

Accounts Payable (AP) is one of the most vulnerable areas of a business when it comes to financial errors, fraud, and unauthorized transactions. Since the AP department is responsible for processing invoices and making payments to vendors, even a small weakness in internal controls can result in significant financial losses. Fraudulent invoices, duplicate payments, fake vendors, and unauthorized transactions can negatively impact a company’s profitability and reputation.

To protect company assets and ensure financial accuracy, businesses must establish strong accounts payable internal controls. Internal controls are policies, procedures, and mechanisms designed to prevent errors, detect irregularities, and ensure that transactions are properly authorized and recorded. Effective AP controls not only reduce fraud risk but also improve operational efficiency, strengthen vendor relationships, and support regulatory compliance.

Internal controls are safeguards that help organizations achieve three primary objectives:

- Protect company assets

- Ensure accurate financial reporting

- Maintain compliance with policies and regulations

In the accounts payable process, internal controls help verify that every purchase is legitimate, properly approved, accurately recorded, and paid only once. A strong control environment creates accountability throughout the entire procurement and payment cycle.

Before discussing preventive measures, it is important to understand the most common types of AP fraud.

Fake Vendor Fraud

One of the most common schemes involves creating fictitious vendors in the accounting system. A dishonest employee may establish a fake supplier and process fraudulent invoices for payment.

Example

An employee creates a vendor called “ABC Office Supplies” and submits fake invoices totaling ₹2,50,000. Since the vendor does not actually exist, the payments are diverted to the employee’s personal account.

Duplicate Payments

Duplicate payments occur when the same invoice is processed more than once due to system errors or weak verification procedures.

Example

Invoice No. INV-1050 is accidentally entered twice and paid twice, resulting in unnecessary cash outflow.

Invoice Manipulation

Fraudsters may alter invoice amounts, bank account details, or payment terms to receive unauthorized funds.

Example

A vendor invoice for ₹50,000 is altered to ₹5,00,000 before approval.

Kickback Schemes

Employees may receive personal benefits from suppliers in exchange for approving inflated invoices or awarding contracts.

Example

A procurement officer intentionally selects an expensive supplier in return for receiving personal commissions.

Unauthorized Purchases

Employees may purchase goods or services without proper approval, leading to unnecessary expenses and budget overruns.

Payment Diversion Fraud

Cybercriminals sometimes impersonate vendors and request changes to banking information.

Example

A fraudster sends an email claiming to be a supplier and requests that future payments be transferred to a new bank account. Without proper verification procedures, the business may unknowingly transfer funds to the fraudster.

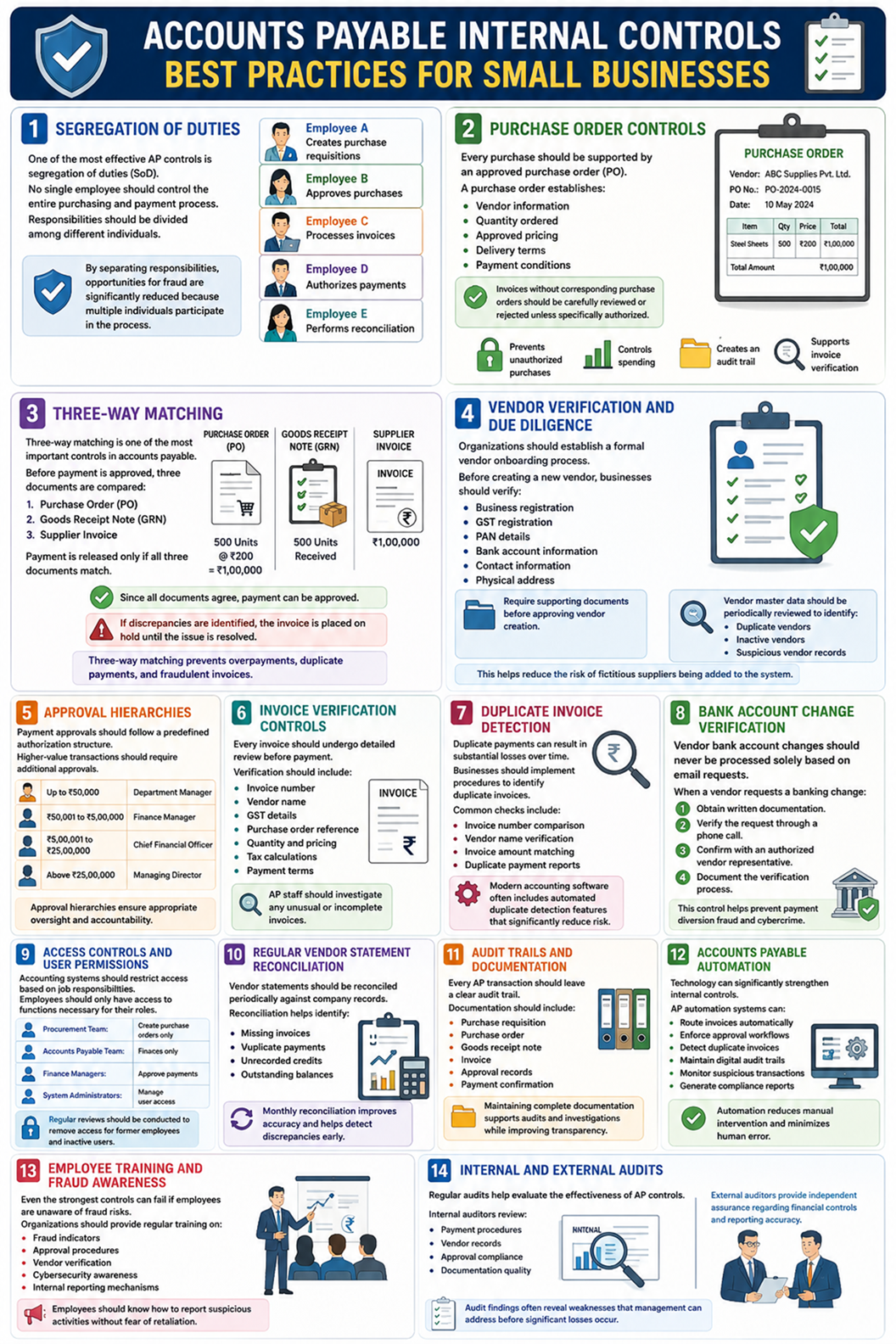

Best Practices for Small Businesses

Segregation of Duties

One of the most effective AP controls is segregation of duties (SoD).

No single employee should control the entire purchasing and payment process.

Responsibilities should be divided among different individuals.

Employee A:

- Creates purchase requisitions

Employee B:

- Approves purchases

Employee C:

- Processes invoices

Employee D:

- Authorizes payments

Employee E:

- Performs reconciliation

By separating responsibilities, opportunities for fraud are significantly reduced because multiple individuals participate in the process.

Purchase Order Controls

Every purchase should be supported by an approved purchase order (PO).

A purchase order establishes:

- Vendor information

- Quantity ordered

- Approved pricing

- Delivery terms

- Payment conditions

Invoices without corresponding purchase orders should be carefully reviewed or rejected unless specifically authorized.

- Prevents unauthorized purchases

- Controls spending

- Creates an audit trail

- Supports invoice verification

Three-Way Matching

Three-way matching is one of the most important controls in accounts payable.

Before payment is approved, three documents are compared:

- Purchase Order (PO)

- Goods Receipt Note (GRN)

- Supplier Invoice

Payment is released only if all three documents match.

Purchase Order:

500 Units @ ₹200 = ₹1,00,000

GRN:

500 Units Received

Invoice:

₹1,00,000

Since all documents agree, payment can be approved.

If discrepancies are identified, the invoice is placed on hold until the issue is resolved.

Three-way matching prevents overpayments, duplicate payments, and fraudulent invoices.

Vendor Verification and Due Diligence

Organizations should establish a formal vendor onboarding process.

Before creating a new vendor, businesses should verify:

- Business registration

- GST registration

- PAN details

- Bank account information

- Contact information

- Physical address

Require supporting documents before approving vendor creation.

Vendor master data should be periodically reviewed to identify:

- Duplicate vendors

- Inactive vendors

- Suspicious vendor records

This helps reduce the risk of fictitious suppliers being added to the system.

Approval Hierarchies

Payment approvals should follow a predefined authorization structure.

Higher-value transactions should require additional approvals.

Up to ₹50,000: Department Manager

₹50,001 to ₹5,00,000: Finance Manager

₹5,00,001 to ₹25,00,000: Chief Financial Officer

Above ₹25,00,000: Managing Director

Approval hierarchies ensure appropriate oversight and accountability.

Invoice Verification Controls

Every invoice should undergo detailed review before payment.

Verification should include:

- Invoice number

- Vendor name

- GST details

- Purchase order reference

- Quantity and pricing

- Tax calculations

- Payment terms

AP staff should investigate any unusual or incomplete invoices.

Duplicate Invoice Detection

Duplicate payments can result in substantial losses over time.

Businesses should implement procedures to identify duplicate invoices.

Common checks include:

- Invoice number comparison

- Vendor name verification

- Invoice amount matching

- Duplicate payment reports

Modern accounting software often includes automated duplicate detection features that significantly reduce risk.

Bank Account Change Verification

Vendor bank account changes should never be processed solely based on email requests.

When a vendor requests a banking change:

- Obtain written documentation.

- Verify the request through a phone call.

- Confirm with an authorized vendor representative.

- Document the verification process.

This control helps prevent payment diversion fraud and cybercrime.

Access Controls and User Permissions

Accounting systems should restrict access based on job responsibilities.

Employees should only have access to functions necessary for their roles.

Procurement Team: Create purchase orders only

Accounts Payable Team: Process invoices only

Finance Managers: Approve payments

System Administrators: Manage user access

Regular reviews should be conducted to remove access for former employees and inactive users.

Regular Vendor Statement Reconciliation

Vendor statements should be reconciled periodically against company records.

Reconciliation helps identify:

- Missing invoices

- Duplicate payments

- Unrecorded credits

- Outstanding balances

Monthly reconciliation improves accuracy and helps detect discrepancies early.

Audit Trails and Documentation

Every AP transaction should leave a clear audit trail.

Documentation should include:

- Purchase requisition

- Purchase order

- Goods receipt note

- Invoice

- Approval records

- Payment confirmation

Maintaining complete documentation supports audits and investigations while improving transparency.

Accounts Payable Automation

Technology can significantly strengthen internal controls.

AP automation systems can:

- Route invoices automatically

- Enforce approval workflows

- Detect duplicate invoices

- Maintain digital audit trails

- Monitor suspicious transactions

- Generate compliance reports

Automation reduces manual intervention and minimizes human error.

Employee Training and Fraud Awareness

Even the strongest controls can fail if employees are unaware of fraud risks.

Organizations should provide regular training on:

- Fraud indicators

- Approval procedures

- Vendor verification

- Cybersecurity awareness

- Internal reporting mechanisms

Employees should know how to report suspicious activities without fear of retaliation.

Internal and External Audits

Regular audits help evaluate the effectiveness of AP controls.

Internal auditors review:

- Payment procedures

- Vendor records

- Approval compliance

- Documentation quality

External auditors provide independent assurance regarding financial controls and reporting accuracy.

Audit findings often reveal weaknesses that management can address before significant losses occur.

Conclusion

Accounts payable is far more than simply paying vendor bills. It is a critical financial process that affects cash flow, supplier relationships, financial reporting, compliance, and business efficiency.

A well-structured accounts payable process includes purchase requests, approvals, purchase orders, invoice verification, three-way matching, payment scheduling, and proper accounting entries. By following a standardized process, businesses can reduce errors, prevent fraud, improve vendor satisfaction, and maintain healthy financial operations.

As businesses continue to embrace digital transformation, modern accounts payable automation solutions are helping finance teams process invoices faster, improve accuracy, and gain greater visibility into organizational spending.