Every successful business relies on accurate financial management to maintain profitability, comply with regulations, and make informed decisions. Two terms that are often used interchangeably in financial management are accounting and bookkeeping. While they are closely related and work together to support a company’s financial operations, they are not the same.

Bookkeeping focuses on recording and organizing financial transactions, whereas accounting involves analyzing, interpreting, and reporting financial information. In simple terms, bookkeeping creates the foundation upon which accounting is built.

For business owners, entrepreneurs, startups, and finance professionals, understanding the distinction between accounting and bookkeeping is essential. Knowing how these functions differ can help businesses allocate resources effectively, improve financial accuracy, and ensure compliance with tax and reporting requirements.

This comprehensive guide explores bookkeeping and accounting in detail, highlights their differences, explains how they work together, and helps businesses determine when they need bookkeeping services, accounting services, or both.

What Is Bookkeeping?

Bookkeeping is the process of systematically recording and organizing a company’s daily financial transactions. It serves as the first step in the accounting cycle and ensures that all financial data is accurately captured.

Bookkeepers maintain detailed records of every financial transaction that occurs within a business, including:

- Sales revenue

- Customer payments

- Vendor payments

- Purchases

- Payroll transactions

- Bank deposits

- Loan payments

- Business expenses

The primary objective of bookkeeping is to create an accurate financial record that accountants can later analyze and interpret.

Key Functions of Bookkeeping

Recording Financial Transactions

Bookkeepers document every financial activity using accounting software, spreadsheets, or bookkeeping systems.

Maintaining General Ledger

The General Ledger serves as the central repository for all financial transactions.

Managing Accounts Receivable

Bookkeepers track customer invoices and payments.

Managing Accounts Payable

They monitor vendor bills and ensure timely payments.

Bank Reconciliation

Bookkeepers compare company records with bank statements to identify discrepancies.

Payroll Processing

Many bookkeepers assist with employee payroll and tax withholding records.

Financial Data Organization

Bookkeepers ensure all financial documents are properly maintained and categorized.

What Is Accounting?

Accounting is the process of analyzing, summarizing, interpreting, and reporting financial information generated through bookkeeping activities.

Accountants use bookkeeping records to evaluate a company’s financial health and provide insights that support decision-making.

Accounting goes beyond recording transactions by transforming raw financial data into meaningful business intelligence.

Key Functions of Accounting

Financial Statement Preparation

Accountants prepare:

- Income Statements

- Balance Sheets

- Cash Flow Statements

- Statements of Equity

Financial Analysis

Accountants evaluate profitability, liquidity, and operational efficiency.

Budgeting and Forecasting

They help businesses plan future expenditures and revenue growth.

Tax Planning and Compliance

Accountants ensure compliance with federal, state, and local tax laws.

Financial Reporting

They prepare reports for management, investors, lenders, and regulatory agencies.

Strategic Advisory Services

Accountants provide recommendations for improving profitability and financial performance.

Internal Control Evaluation

They identify risks and implement controls to reduce fraud and errors.

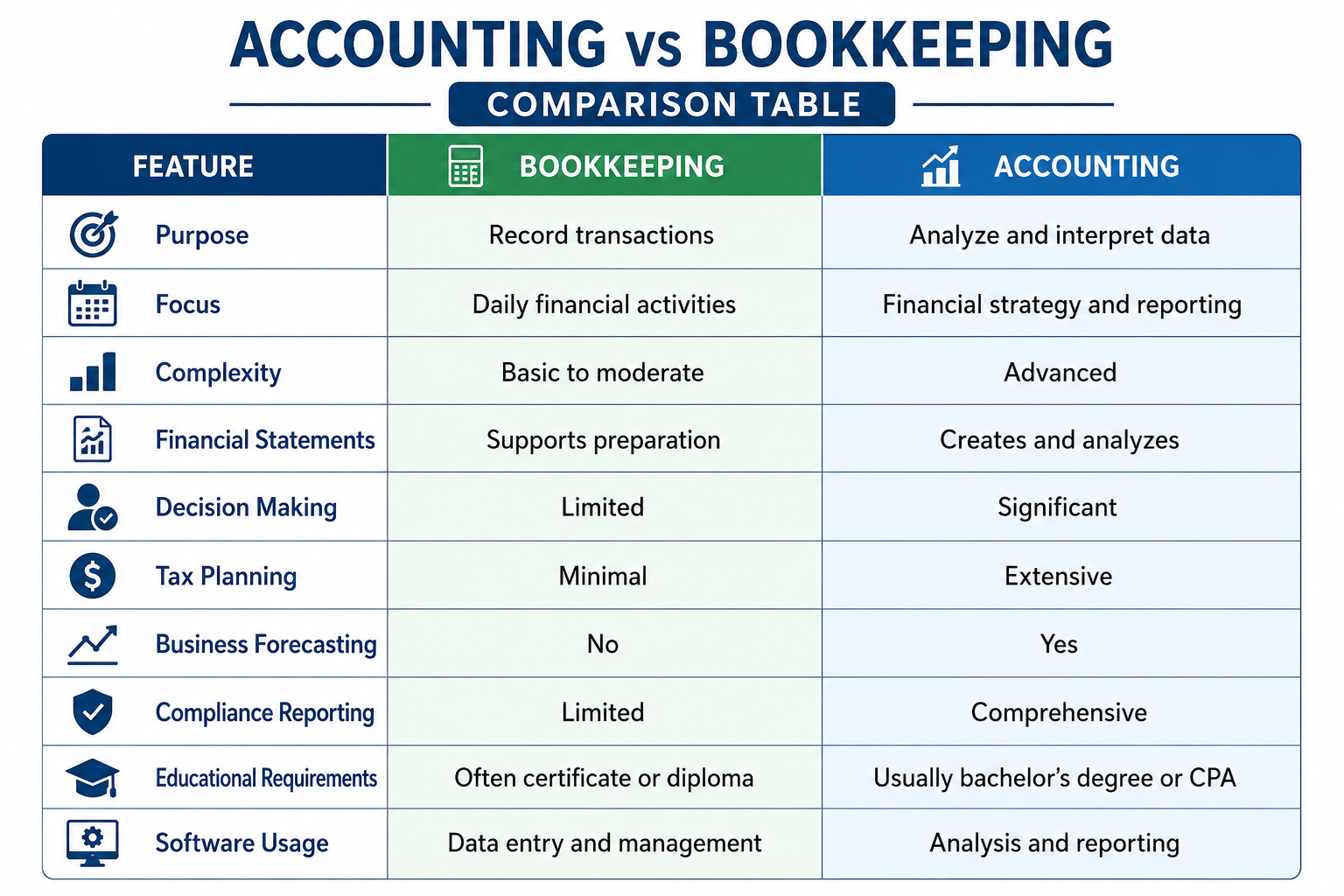

Accounting vs Bookkeeping: The Core Difference

The simplest way to understand the difference is:

Bookkeeping records financial data.

Accounting interprets financial data.

Bookkeeping focuses on collecting financial information, while accounting focuses on using that information to support decision-making.

Without bookkeeping, accountants would have no reliable financial data to analyze.

Without accounting, businesses would have no meaningful interpretation of their financial records.

Accounting vs Bookkeeping Comparison Table

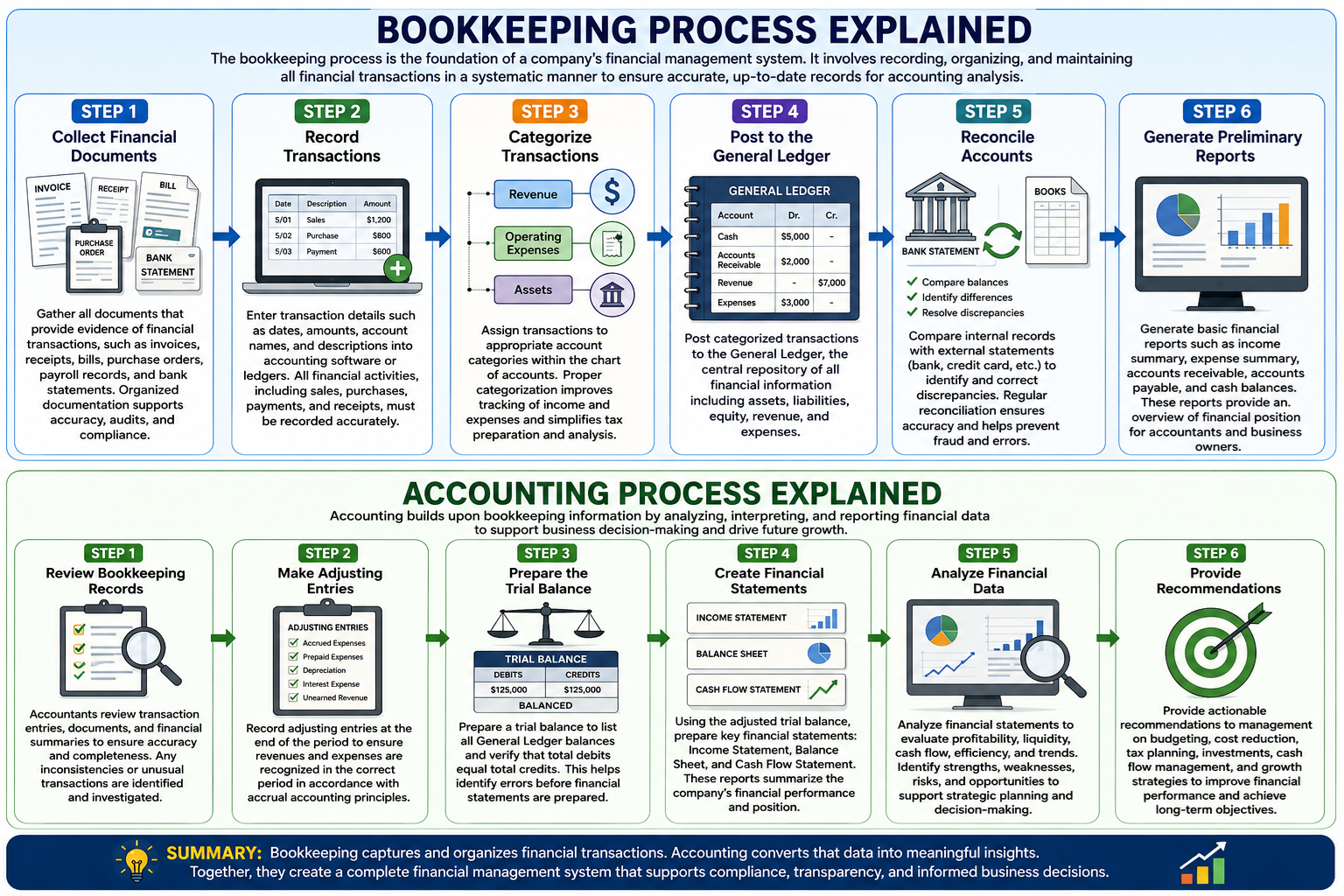

Bookkeeping Process Explained

The bookkeeping process is the foundation of a company’s financial management system. It involves recording, organizing, and maintaining all financial transactions in a systematic manner. Accurate bookkeeping ensures that financial records are complete, up-to-date, and ready for accounting analysis. The bookkeeping process typically consists of the following steps:

Step 1: Collect Financial Documents

The first step in bookkeeping is gathering all documents that provide evidence of financial transactions. These documents serve as the source records used to enter financial information into the accounting system. Common financial documents include invoices issued to customers, receipts for purchases, vendor bills, purchase orders, payroll records, and bank statements. Maintaining organized documentation is essential because it helps verify transactions, supports audits, and ensures compliance with financial regulations.

Step 2: Record Transactions

Once financial documents are collected, the transactions are recorded in the bookkeeping system. This process involves entering details such as transaction dates, amounts, account names, and descriptions into accounting software or bookkeeping ledgers. Every financial activity, including sales, purchases, payments, and receipts, must be recorded accurately. Proper transaction recording ensures that the company’s financial records reflect its actual business activities.

Step 3: Categorize Transactions

After transactions are recorded, they are assigned to appropriate account categories within the chart of accounts. For example, utility payments may be categorized as operating expenses, while customer payments are recorded as revenue. Proper categorization helps businesses track income and expenses effectively and makes financial reporting more accurate. It also simplifies tax preparation and financial analysis.

Step 4: Post to the General Ledger

The categorized transactions are then posted to the General Ledger, which serves as the central repository of all financial information. The General Ledger contains separate accounts for assets, liabilities, equity, revenue, and expenses. Posting transactions to the General Ledger ensures that every financial event is properly reflected in the company’s accounting records and contributes to accurate financial reporting.

Step 5: Reconcile Accounts

Account reconciliation involves comparing internal financial records with external statements, such as bank statements and credit card statements. The purpose of reconciliation is to identify and correct discrepancies, including missing transactions, duplicate entries, bank errors, or unauthorized charges. Regular reconciliation helps maintain the accuracy of financial records and reduces the risk of fraud and accounting mistakes.

Step 6: Generate Preliminary Reports

Once transactions have been recorded, categorized, and reconciled, basic financial reports can be generated. These reports may include summaries of income, expenses, accounts receivable, accounts payable, and cash balances. Preliminary reports provide accountants and business owners with an overview of the company’s financial position and serve as the starting point for more detailed accounting analysis.

Accounting Process Explained

Accounting builds upon the information created through bookkeeping. While bookkeeping focuses on recording transactions, accounting involves analyzing, interpreting, and reporting financial data to support business decision-making. The accounting process transforms raw financial information into meaningful insights that help businesses evaluate performance and plan for the future.

Step 1: Review Bookkeeping Records

The accounting process begins with a thorough review of bookkeeping records. Accountants examine transaction entries, supporting documents, and financial summaries to ensure that all information is accurate and complete. Any inconsistencies, missing entries, or unusual transactions are identified and investigated. This review helps establish a reliable foundation for financial reporting.

Step 2: Make Adjusting Entries

At the end of an accounting period, accountants make adjusting entries to ensure that revenues and expenses are recorded in the correct period. These adjustments may include accrued expenses, prepaid expenses, depreciation, interest expenses, and unearned revenue. Adjusting entries are necessary to comply with accrual accounting principles and provide a more accurate representation of the company’s financial position.

Step 3: Prepare the Trial Balance

After adjustments are made, accountants prepare a trial balance. A trial balance is a report that lists all General Ledger account balances and verifies that total debits equal total credits. This step helps identify posting errors, calculation mistakes, or other discrepancies before financial statements are prepared. A balanced trial balance is an important indicator of accounting accuracy.

Step 4: Create Financial Statements

Using the adjusted trial balance, accountants prepare key financial statements that summarize the company’s financial performance and position. These statements typically include the Income Statement, Balance Sheet, and Cash Flow Statement. Financial statements provide valuable information to business owners, investors, lenders, regulators, and other stakeholders.

Step 5: Analyze Financial Data

Once financial statements are prepared, accountants analyze the information to evaluate business performance. They review profitability, liquidity, cash flow, operational efficiency, and financial trends. Financial analysis helps identify strengths, weaknesses, risks, and opportunities within the business. This information supports better strategic planning and decision-making.

Step 6: Provide Recommendations

The final step in the accounting process is providing recommendations based on financial analysis. Accountants use their findings to advise management on budgeting, cost reduction, tax planning, investment decisions, cash flow management, and business growth strategies. These recommendations help organizations improve financial performance and achieve long-term objectives.

In summary, bookkeeping focuses on accurately recording financial transactions, while accounting transforms that financial data into actionable insights. Together, these processes create a complete financial management system that supports compliance, transparency, and informed business decision-making.

Skills Required for Bookkeeping

Successful bookkeepers typically possess:

Attention to Detail

Small errors can affect financial accuracy.

Organizational Skills

Managing large volumes of financial data requires structure.

Basic Accounting Knowledge

Understanding debits and credits is essential.

Software Proficiency

Knowledge of accounting software is critical.

Time Management

Meeting deadlines is important.

Communication Skills

Bookkeepers frequently interact with clients and vendors.

Skills Required for Accounting

Accountants generally need:

Analytical Thinking

Financial data must be interpreted accurately.

Problem-Solving Skills

Complex financial issues require solutions.

Tax Knowledge

Understanding tax regulations is crucial.

Regulatory Knowledge

Compliance requirements must be followed.

Financial Reporting Expertise

Accurate reporting is essential.

Strategic Planning Abilities

Accountants help guide business growth.

Educational Requirements: Accounting vs Bookkeeping

Bookkeeper Education

Many bookkeepers have:

- High school diploma

- Associate degree

- Bookkeeping certificate

- Software certifications

Accountant Education

Most accountants possess:

- Bachelor’s degree in Accounting

- Finance degree

- CPA certification

- Advanced accounting credentials

How Accounting and Bookkeeping Work Together

Bookkeeping and accounting are complementary functions.

Bookkeepers

- Record transactions

- Maintain ledgers

- Organize financial records

Accountants

- Analyze records

- Prepare reports

- Provide insights

- Ensure compliance

Without bookkeeping, accounting cannot function effectively.

Without accounting, bookkeeping data has limited strategic value.

When Does a Business Need a Bookkeeper?

A business should consider hiring a bookkeeper when:

- Transaction volume increases

- Payroll becomes complex

- Invoices are difficult to track

- Financial records become disorganized

- Tax season becomes stressful

When Does a Business Need an Accountant?

Businesses often require an accountant when:

- Preparing tax returns

- Seeking financing

- Planning expansion

- Managing complex finances

- Preparing financial statements

- Conducting audits

Small Business Accounting vs Bookkeeping

Small businesses often start with basic bookkeeping.

As businesses grow, accounting becomes increasingly important.

Startups

Usually require bookkeeping first.

Growing Businesses

Need both bookkeeping and accounting support.

Large Organizations

Maintain separate bookkeeping and accounting departments.

Real-World Example: Accounting vs Bookkeeping

Imagine a retail store sells products worth $10,000 during a month.

Bookkeeper’s Role

- Records each sale

- Updates customer accounts

- Reconciles bank deposits

- Records inventory purchases

Accountant’s Role

- Analyzes profitability

- Calculates gross margin

- Prepares financial statements

- Identifies cost-saving opportunities

- Assesses future growth projections

The bookkeeper records the transaction.

The accountant explains what the transaction means for the business.

Conclusion

Although accounting and bookkeeping are closely connected, they serve distinct purposes within a business. Bookkeeping focuses on accurately recording and organizing financial transactions, while accounting analyzes, interprets, and reports financial information to support business decisions.

Together, these functions create a complete financial management system. Bookkeeping provides the foundation, and accounting transforms financial records into actionable insights. Businesses of all sizes—from startups to large enterprises—benefit from both disciplines.

Understanding the differences between accounting and bookkeeping helps business owners make informed decisions, improve financial accuracy, maintain compliance, and build a stronger foundation for long-term growth.

Frequently Asked Questions (FAQs)

- What is the main difference between accounting and bookkeeping?

Bookkeeping records transactions, while accounting analyzes and interprets financial data.

- Is bookkeeping part of accounting?

Yes. Bookkeeping is the first step in the accounting process.

- Can a bookkeeper prepare financial statements?

Some bookkeepers can generate basic reports, but accountants typically prepare and analyze official financial statements.

- Do small businesses need both bookkeeping and accounting?

Yes. Both functions support financial accuracy and informed decision-making.

- Which comes first, bookkeeping or accounting?

Bookkeeping always comes first.