Managing finances is one of the most important responsibilities for any small business owner. Whether you run a local retail store, a service-based company, an online business, or a growing startup, accurate financial records help you understand your business’s performance, stay compliant with tax regulations, and make informed decisions.

One of the most reliable and widely used accounting systems in the world is double-entry bookkeeping. While the term may sound complicated, the concept is straightforward once you understand the fundamentals.

Double-entry bookkeeping is the foundation of modern accounting. It provides a structured way to record every financial transaction and helps ensure that your books remain accurate and balanced. Most accounting software platforms used by small businesses today—including QuickBooks, Xero, FreshBooks, and Sage—are built on double-entry accounting principles.

In this guide, we’ll explain what double-entry bookkeeping is, how it works, why it matters for small businesses, and how you can implement it effectively.

What Is Double-Entry Bookkeeping?

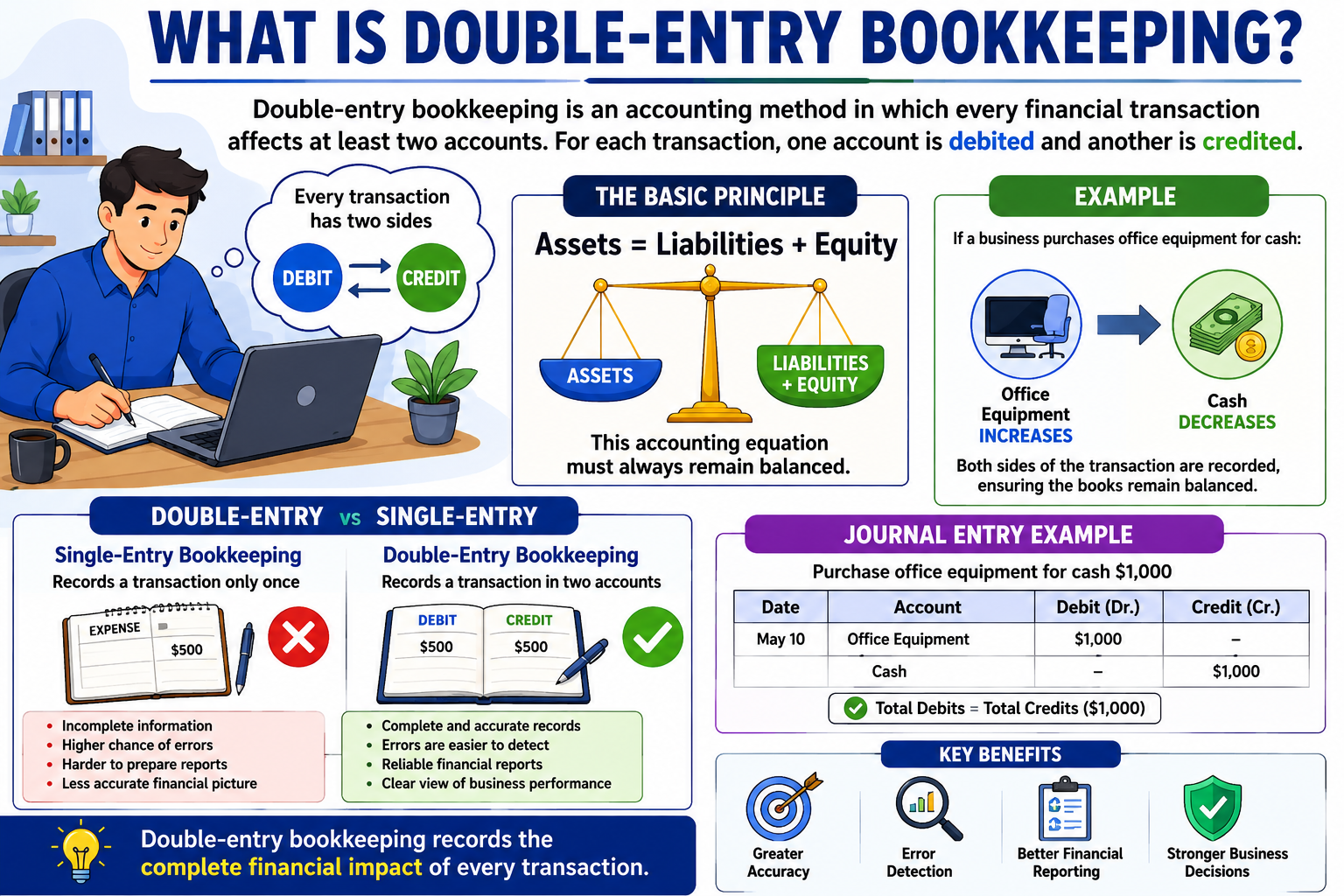

Double-entry bookkeeping is an accounting method in which every financial transaction affects at least two accounts. For each transaction, one account is debited and another account is credited. The system is based on a simple principle:

Assets = Liabilities + Equity

This accounting equation must always remain balanced. Every transaction recorded in the books maintains this balance by creating equal and opposite entries.

For example, if a business purchases office equipment for cash:

- Office Equipment account increases

- Cash account decreases

Both sides of the transaction are recorded, ensuring the books remain balanced.

Unlike single-entry bookkeeping, where transactions are recorded only once, double-entry bookkeeping records the complete financial impact of every transaction.

The History of Double-Entry Bookkeeping

Double-entry bookkeeping has been used for centuries. The system was formally documented by Italian mathematician and Franciscan friar Luca Pacioli in 1494.

Pacioli’s work introduced accounting concepts that remain relevant today. Because of his contributions, he is often referred to as the “Father of Accounting.”

Although accounting software has transformed how bookkeeping is performed, the underlying principles of double-entry accounting have remained largely unchanged for more than 500 years.

Why Small Businesses Need Double-Entry Bookkeeping

Many small business owners start with spreadsheets or simple income-and-expense tracking systems. While this may work temporarily, businesses often outgrow these methods.

Double-entry bookkeeping offers several advantages.

- Greater Accuracy

Since every transaction requires at least two entries, errors become easier to identify.

If debits and credits do not balance, it signals that something is wrong and needs investigation.

This built-in verification system reduces mistakes and improves financial accuracy.

- Better Financial Reporting

Double-entry accounting provides the information needed to create:

- Balance sheets

- Income statements

- Cash flow statements

- Financial forecasts

These reports help owners understand profitability and financial health.

- Easier Tax Preparation

Accurate records simplify tax filing and reduce the risk of reporting errors.

When all transactions are properly categorized and documented, accountants can prepare returns more efficiently.

- Improved Business Decision-Making

Reliable financial data helps owners answer important questions such as:

- Are we profitable?

- Can we afford to hire employees?

- Should we invest in new equipment?

- How much cash do we have available?

Without accurate bookkeeping, these decisions become guesswork.

- Increased Credibility

Banks, investors, and lenders often require professional financial statements.

Double-entry bookkeeping helps create the financial transparency needed to secure funding and build trust.

Understanding Debits and Credits

One of the biggest sources of confusion for beginners is understanding debits and credits.

Many people assume:

- Debit = bad

- Credit = good

In accounting, that’s not true.

Debits and credits simply indicate whether an account increases or decreases.

Debit (Dr)

A debit increases:

- Assets

- Expenses

A debit decreases:

- Liabilities

- Equity

- Revenue

Credit (Cr)

A credit increases:

- Liabilities

- Equity

- Revenue

A credit decreases:

- Assets

- Expenses

The key rule is:

Total Debits = Total Credits

Every transaction must balance.

The Five Main Types of Accounts

To understand double-entry bookkeeping, you need to know the five major account categories.

- Assets

Assets are resources owned by the business.

Examples include:

- Cash

- Inventory

- Equipment

- Vehicles

- Accounts receivable

- Buildings

Assets generally increase with debits and decrease with credits.

- Liabilities

Liabilities represent money owed to others.

Examples include:

- Business loans

- Credit card balances

- Accounts payable

- Payroll taxes payable

Liabilities increase with credits and decrease with debits.

- Equity

Equity represents the owner’s interest in the business.

Examples include:

- Owner contributions

- Retained earnings

- Common stock

Equity increases with credits and decreases with debits.

- Revenue

Revenue represents money earned through business operations.

Examples include:

- Product sales

- Service income

- Consulting fees

Revenue increases with credits.

- Expenses

Expenses represent the cost of running the business.

Examples include:

- Rent

- Payroll

- Utilities

- Advertising

- Office supplies

Expenses increase with debits.

How Double-Entry Bookkeeping Works

Let’s examine a few common business transactions.

Example 1: Owner Invests Cash

A business owner contributes $20,000 to start the company.

Entry

Debit:

- Cash = $20,000

Credit:

- Owner’s Equity = $20,000

Result:

- Assets increase

- Equity increases

Books remain balanced.

Example 2: Purchasing Equipment

The company buys a computer for $2,000 cash.

Entry

Debit:

- Equipment = $2,000

Credit:

- Cash = $2,000

Result:

- Equipment increases

- Cash decreases

Net assets remain balanced.

Example 3: Making a Sale

A business sells services worth $1,500 and receives payment immediately.

Entry

Debit:

- Cash = $1,500

Credit:

- Revenue = $1,500

Result:

- Cash increases

- Revenue increases

Example 4: Paying Rent

The company pays monthly rent of $1,000.

Entry

Debit:

- Rent Expense = $1,000

Credit:

- Cash = $1,000

Result:

- Expense increases

- Cash decreases

Example 5: Taking a Loan

The business receives a $50,000 bank loan.

Entry

Debit:

- Cash = $50,000

Credit:

- Loan Payable = $50,000

Result:

- Assets increase

- Liabilities increase

Books remain balanced.

Double-Entry vs. Single-Entry Bookkeeping

Many small businesses begin with single-entry bookkeeping.

Let’s compare both methods.

| Feature | Single-Entry | Double-Entry |

| Records transactions once | Yes | No |

| Records full transaction impact | No | Yes |

| Tracks assets and liabilities | Limited | Yes |

| Produces financial statements | Difficult | Easy |

| Error detection | Weak | Strong |

| Suitable for growing businesses | Limited | Yes |

Single-entry systems may work for freelancers or hobby businesses with very few transactions.

However, once a business begins growing, double-entry bookkeeping becomes essential.

The Accounting Equation Explained

At the heart of double-entry bookkeeping lies the accounting equation:

Assets = Liabilities + Equity

This equation reflects the financial position of a business.

For example:

Assets:

- Cash: $30,000

- Equipment: $20,000

Total Assets = $50,000

Liabilities:

- Loan: $15,000

Owner Equity:

- $35,000

Liabilities + Equity = $50,000

The equation balances perfectly.

Every transaction must preserve this balance.

What Is a Chart of Accounts?

A chart of accounts is a structured list of all accounts used by a business.

It acts as the backbone of the bookkeeping system.

Typical categories include:

Assets

- Checking Account

- Savings Account

- Accounts Receivable

- Inventory

- Equipment

Liabilities

- Credit Cards

- Business Loans

- Accounts Payable

Equity

- Owner Capital

- Retained Earnings

Revenue

- Sales Revenue

- Service Revenue

Expenses

- Rent Expense

- Utilities Expense

- Marketing Expense

- Payroll Expense

A well-organized chart of accounts improves reporting and bookkeeping efficiency.

Journal Entries in Double-Entry Accounting

Every transaction is first recorded in a journal.

A journal entry includes:

- Date

- Accounts affected

- Debit amount

- Credit amount

- Description

Example:

Date: June 1

| Account | Debit | Credit |

| Cash | $5,000 | |

| Sales Revenue | $5,000 |

Description:

Service revenue received from customer.

These journal entries are later posted to the general ledger.

What Is the General Ledger?

The general ledger is the central repository of all financial transactions.

It contains every account in the chart of accounts.

Think of the general ledger as the master database of your business finances.

Accountants use the general ledger to:

- Track balances

- Generate reports

- Reconcile accounts

- Prepare financial statements

Modern accounting software automatically updates the general ledger whenever transactions are entered.

Common Double-Entry Bookkeeping Mistakes

Even with a strong system, errors can occur.

Some common mistakes include:

Recording Transactions in the Wrong Account

For example:

Recording equipment purchases as office supplies.

This can distort financial statements.

Missing Transactions

Failing to record transactions creates incomplete records and inaccurate reports.

Duplicate Entries

Entering the same transaction twice can overstate income or expenses.

Incorrect Debit or Credit Entries

Misclassifying debits and credits can cause account balances to become inaccurate.

Poor Reconciliation Practices

Failing to reconcile bank accounts regularly can allow errors to go unnoticed.

How Accounting Software Uses Double-Entry Bookkeeping

Most modern accounting platforms automatically apply double-entry principles.

For example, when you create an invoice:

- Accounts Receivable increases

- Revenue increases

When the customer pays:

- Cash increases

- Accounts Receivable decreases

The software creates the necessary journal entries behind the scenes.

This automation reduces manual work while maintaining accounting accuracy.