Running a business in the United States requires much more than offering great products or services. Every business owner, whether operating a startup, a small business, or a growing company, must understand basic accounting concepts. While you don’t need to become a certified accountant, knowing key accounting terms can help you make smarter financial decisions, improve profitability, maintain compliance, and communicate effectively with bookkeepers, accountants, investors, and lenders.

Many entrepreneurs focus heavily on sales and marketing while overlooking financial management. However, understanding accounting terminology can provide valuable insight into your company’s financial health. These terms appear in financial statements, tax documents, bookkeeping software, loan applications, and business reports.

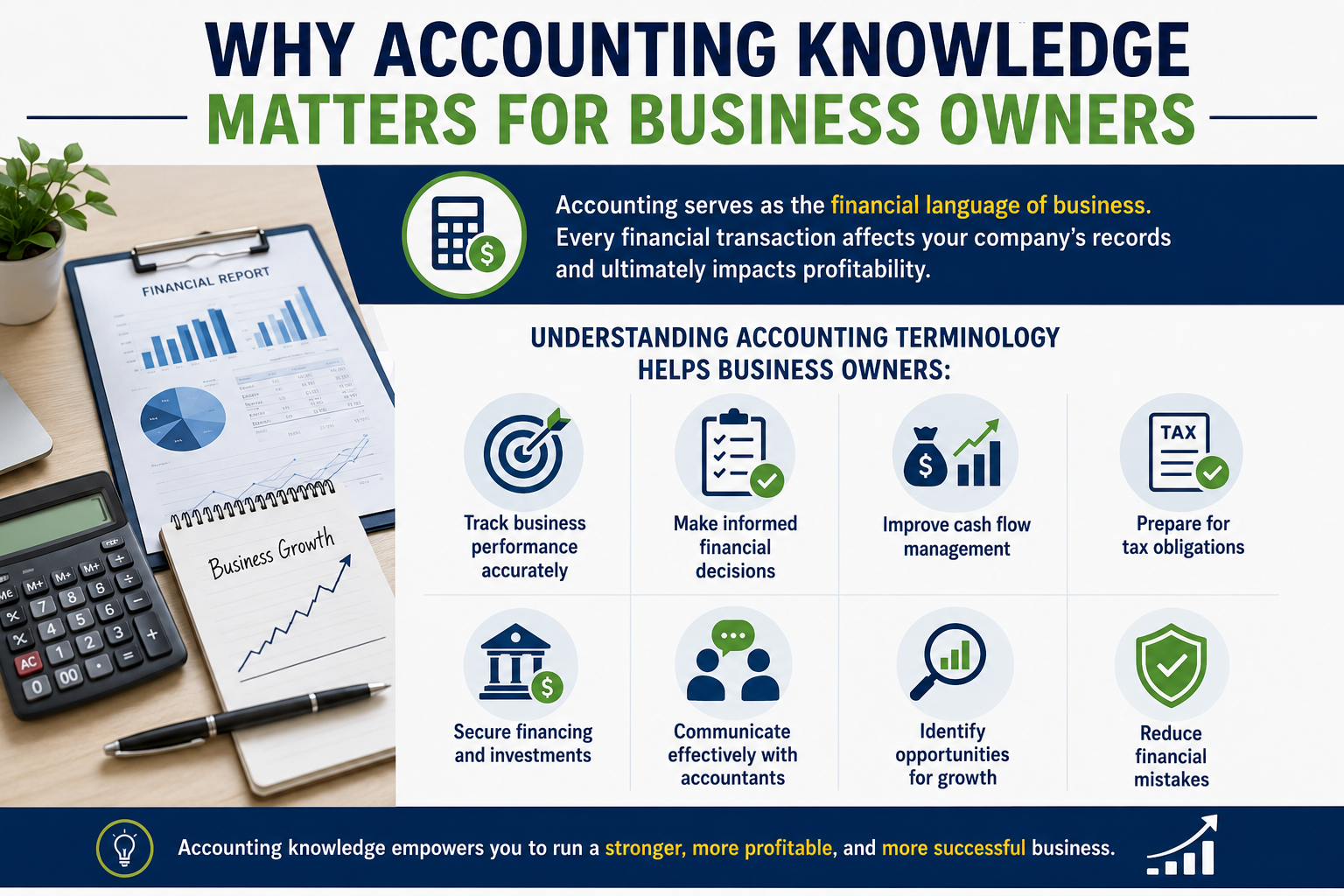

This guide explains the most important accounting terms every business owner should know. By understanding these concepts, you’ll be better equipped to monitor performance, manage cash flow, reduce risks, and grow your business confidently.

Why Accounting Knowledge Matters for Business Owners

Let’s explore the essential accounting terms every business owner should understand.

- Assets

Assets are resources owned by a business that provide future economic value.

In simple terms, assets are things your company owns that can generate income or be converted into cash.

Examples include:

- Cash

- Inventory

- Equipment

- Vehicles

- Buildings

- Accounts receivable

- Investments

Assets are generally divided into two categories:

Current Assets

Current assets can be converted into cash within one year.

Examples:

- Cash

- Inventory

- Accounts receivable

- Short-term investments

Non-Current Assets

Long-term assets that provide value beyond one year.

Examples:

- Machinery

- Real estate

- Vehicles

- Patents

Understanding assets helps business owners evaluate financial strength and operational capacity.

- Liabilities

Liabilities represent money your business owes to others.

These obligations must be paid in the future.

Examples include:

- Business loans

- Credit card balances

- Vendor invoices

- Payroll taxes

- Mortgage payments

Liabilities are classified as:

Current Liabilities

Due within one year.

Examples:

- Accounts payable

- Short-term loans

- Payroll obligations

Long-Term Liabilities

Due after one year.

Examples:

- Commercial mortgages

- Equipment financing

- Long-term business loans

Monitoring liabilities helps ensure your business remains financially stable.

- Equity

Equity represents the owner’s ownership interest in a business.

It is calculated using the accounting equation:

Assets – Liabilities = Equity

If your business owns $500,000 in assets and owes $200,000 in liabilities, your equity equals $300,000.

Equity may include:

- Owner contributions

- Retained earnings

- Common stock

- Additional paid-in capital

Investors often examine equity when evaluating a company’s financial health.

- Revenue

Revenue refers to income generated from normal business operations.

It is often called:

- Sales

- Gross income

- Top-line revenue

Examples include:

- Product sales

- Service income

- Subscription fees

- Consulting fees

Revenue is not the same as profit.

A business can generate substantial revenue while still losing money if expenses exceed income.

- Expenses

Expenses are costs incurred while operating a business.

Common business expenses include:

- Rent

- Utilities

- Salaries

- Marketing

- Insurance

- Office supplies

- Software subscriptions

Tracking expenses accurately helps improve profitability and supports tax deductions.

- Profit

Profit represents the amount remaining after expenses are subtracted from revenue.

Formula:

Profit = Revenue – Expenses

Profit indicates whether your business is making money.

Businesses typically monitor:

Gross Profit

Revenue minus cost of goods sold.

Operating Profit

Profit after operating expenses.

Net Profit

Final profit after all expenses and taxes.

Net profit is often considered the most important profitability metric.

- Cost of Goods Sold (COGS)

COGS refers to the direct costs associated with producing goods sold by a business.

Examples include:

- Raw materials

- Manufacturing labor

- Packaging

- Production supplies

For retailers, COGS generally equals inventory purchased for resale.

Formula:

COGS = Beginning Inventory + Purchases – Ending Inventory

Accurate COGS calculations help determine gross profit.

- Gross Profit

Gross profit measures profitability before operating expenses.

Formula:

Gross Profit = Revenue – COGS

Example:

Revenue: $100,000

COGS: $40,000

Gross Profit: $60,000

Gross profit helps business owners evaluate pricing strategies and production efficiency.

- Net Income

Net income represents the company’s final earnings after all expenses, taxes, interest, and costs have been deducted.

It is often called:

- Bottom line

- Net earnings

- Profit after tax

Formula:

Net Income = Revenue – Total Expenses

Positive net income generally indicates financial success.

- Accounts Receivable (AR)

Accounts receivable represents money customers owe your business.

If you provide services before receiving payment, the unpaid invoice becomes an account receivable.

Example:

A marketing agency invoices a client for $5,000 with net-30 payment terms.

The $5,000 is recorded as accounts receivable until payment is received.

High accounts receivable balances may create cash flow challenges.

- Accounts Payable (AP)

Accounts payable refers to money your business owes vendors and suppliers.

Example:

A supplier sends inventory worth $10,000 with payment due in 30 days.

The amount is recorded as accounts payable.

Managing AP effectively helps maintain strong supplier relationships and healthy cash flow.

- Cash Flow

Cash flow measures money moving into and out of a business.

Positive cash flow means more money enters than leaves.

Negative cash flow means expenses exceed incoming cash.

Cash flow is often more important than profit because businesses can fail even when profitable if they run out of cash.

Three types include:

- Operating cash flow

- Investing cash flow

- Financing cash flow

Successful businesses closely monitor cash flow every month.

- Accounts Receivable Turnover

This metric measures how quickly customers pay invoices.

Formula:

Net Credit Sales ÷ Average Accounts Receivable

Higher turnover generally indicates faster collections.

Slow collections may create financial stress.

Business owners should establish clear payment policies to improve receivable turnover.

- Depreciation

Depreciation spreads the cost of a long-term asset over its useful life.

Example:

A company purchases equipment for $50,000 expected to last 10 years.

Instead of recording the entire expense immediately, depreciation allocates the cost over multiple years.

Benefits include:

- More accurate financial reporting

- Tax advantages

- Better matching of expenses to revenue

- Amortization

Amortization is similar to depreciation but applies to intangible assets.

Examples include:

- Patents

- Trademarks

- Copyrights

- Software licenses

If a business purchases a patent, the cost may be amortized over its useful life.

This helps distribute expenses fairly across accounting periods.

- Inventory

Inventory consists of products a business intends to sell.

Inventory may include:

- Raw materials

- Work-in-progress goods

- Finished products

Inventory management directly affects profitability.

Too much inventory can tie up cash.

Too little inventory may result in lost sales.

Effective inventory control helps maintain healthy cash flow.

- Working Capital

Working capital measures short-term financial health.

Formula:

Current Assets – Current Liabilities

Positive working capital indicates the business can meet short-term obligations.

Negative working capital may signal financial difficulties.

Lenders often review working capital before approving financing.

- General Ledger

The general ledger is the central repository of all financial transactions.

Every accounting entry eventually flows into the general ledger.

It contains information about:

- Assets

- Liabilities

- Revenue

- Expenses

- Equity

Modern accounting software automatically updates the general ledger.

- Journal Entry

A journal entry records a financial transaction.

Each entry typically includes:

- Date

- Accounts affected

- Debit amount

- Credit amount

- Description

Journal entries form the foundation of bookkeeping.

Accurate entries ensure reliable financial statements.

- Double-Entry Accounting

Double-entry accounting is the standard accounting system used by businesses worldwide.

Every transaction affects at least two accounts.

For every debit, there is an equal credit.

Example:

Buying equipment with cash:

- Debit Equipment

- Credit Cash

This system helps maintain accurate and balanced financial records.

- Balance Sheet

The balance sheet provides a snapshot of financial position at a specific date.

It includes:

- Assets

- Liabilities

- Equity

The balance sheet follows the accounting equation:

Assets = Liabilities + Equity

Business owners use balance sheets to evaluate financial stability and solvency.

- Income Statement

The income statement reports profitability over a specific period.

It includes:

- Revenue

- Expenses

- Gross profit

- Operating income

- Net income

This statement helps owners determine whether the business is generating profits.

- Cash Flow Statement

The cash flow statement tracks actual cash movement.

It is divided into:

- Operating activities

- Investing activities

- Financing activities

Many profitable companies experience cash shortages due to poor cash flow management.

The cash flow statement reveals these issues.

- Bookkeeping

Bookkeeping is the process of recording, organizing, and maintaining a company’s financial transactions.

While accounting focuses on analyzing financial data and preparing reports, bookkeeping focuses on collecting and recording financial information.

Common bookkeeping tasks include:

- Recording sales

- Tracking expenses

- Managing invoices

- Reconciling bank accounts

- Processing payroll

Accurate bookkeeping is essential because all financial reports depend on the quality of the underlying records.

- Fiscal Year

A fiscal year is a 12-month accounting period used for financial reporting and tax purposes.

Many small businesses use the calendar year:

- January 1 to December 31

However, some companies choose a different fiscal year based on operational needs.

For example:

- July 1 to June 30

- October 1 to September 30

Understanding your fiscal year is important for budgeting, tax planning, and financial reporting.

- Accrual Accounting

Accrual accounting records revenue when earned and expenses when incurred, regardless of when cash changes hands.

Example:

A consulting firm completes a project in December but receives payment in January.

Under accrual accounting:

- Revenue is recorded in December.

This method provides a more accurate picture of financial performance.

Many growing businesses and corporations use accrual accounting because it aligns income and expenses with the period in which they occur.

- Cash Basis Accounting

Cash basis accounting records transactions only when money is received or paid.

Example:

Revenue is recorded when a customer pays an invoice.

Expenses are recorded when bills are paid.

Advantages include:

- Simplicity

- Easier bookkeeping

- Straightforward tax reporting

Many small businesses begin with cash basis accounting before transitioning to accrual accounting as they grow.

- Bank Reconciliation

Bank reconciliation is the process of comparing internal accounting records with bank statements.

The purpose is to identify discrepancies such as:

- Missing transactions

- Bank fees

- Duplicate entries

- Recording errors

- Fraudulent activity

Regular reconciliations improve financial accuracy and help detect problems early.

- Trial Balance

A trial balance is a report listing all account balances in the general ledger.

Its purpose is to verify that:

Total Debits = Total Credits

If the totals do not match, errors may exist in the accounting records.

The trial balance serves as an important step before preparing financial statements.

- Budget

A budget is a financial plan that estimates future income and expenses.

Businesses use budgets to:

- Set financial goals

- Control spending

- Allocate resources

- Forecast profitability

A budget may include projections for:

- Sales

- Payroll

- Marketing

- Equipment purchases

- Operating expenses

Regularly comparing actual performance against budgeted amounts helps improve decision-making.

- Forecast

A forecast estimates future financial results based on historical data and current trends.

Businesses use forecasts to predict:

- Revenue

- Expenses

- Cash flow

- Profitability

Unlike budgets, forecasts are often updated throughout the year as circumstances change.

Forecasting helps business owners prepare for growth opportunities and economic challenges.

- Break-Even Point

The break-even point is the level of sales required to cover all business costs.

At break-even:

Profit = Zero

Formula:

Fixed Costs ÷ Contribution Margin

Example:

If fixed costs equal $50,000 and each sale contributes $50 toward fixed costs, the business must generate 1,000 sales to break even.

Understanding the break-even point helps business owners make pricing and growth decisions.

- Fixed Costs

Fixed costs remain relatively constant regardless of production levels.

Examples include:

- Rent

- Insurance

- Salaries

- Property taxes

- Subscription software

Whether a business sells 10 products or 10,000 products, fixed costs generally remain the same.

Monitoring fixed costs helps maintain profitability.

- Variable Costs

Variable costs change based on production or sales volume.

Examples include:

- Raw materials

- Shipping expenses

- Packaging

- Sales commissions

- Manufacturing supplies

As production increases, variable costs increase.

Understanding variable costs helps business owners set profitable pricing strategies.

- Contribution Margin

Contribution margin measures how much revenue remains after variable costs.

Formula:

Sales Revenue – Variable Costs

Contribution margin helps determine:

- Profitability

- Break-even points

- Product performance

Higher contribution margins generally indicate stronger profitability potential.

- Gross Margin

Gross margin measures gross profit as a percentage of revenue.

Formula:

Gross Profit ÷ Revenue × 100

Example:

Revenue = $100,000

Gross Profit = $60,000

Gross Margin = 60%

Gross margin helps evaluate pricing effectiveness and production efficiency.

- Operating Expenses

Operating expenses are costs associated with running day-to-day business operations.

Examples include:

- Rent

- Marketing

- Payroll

- Utilities

- Office supplies

- Insurance

Operating expenses exclude direct production costs.

Business owners should monitor operating expenses carefully to maintain profitability.

- Operating Income

Operating income represents profit generated from core business operations.

Formula:

Gross Profit – Operating Expenses

Operating income excludes:

- Taxes

- Interest expenses

- Extraordinary items

Investors often use operating income to evaluate operational efficiency.

- EBITDA

EBITDA stands for:

Earnings Before Interest, Taxes, Depreciation, and Amortization.

It is commonly used to measure business performance.

Formula:

Net Income

- Interest

- Taxes

- Depreciation

- Amortization

EBITDA helps compare companies by focusing on operational profitability rather than financing and accounting differences.

- Profit Margin

Profit margin measures how much profit remains from each dollar of revenue.

Formula:

Net Income ÷ Revenue × 100

Example:

Revenue = $200,000

Net Income = $20,000

Profit Margin = 10%

Higher profit margins generally indicate stronger financial performance.

- Liquidity

Liquidity refers to a company’s ability to meet short-term financial obligations.

Highly liquid assets can be quickly converted into cash.

Examples include:

- Cash

- Savings accounts

- Marketable securities

Strong liquidity helps businesses handle unexpected expenses and economic downturns.

- Solvency

Solvency measures a company’s ability to meet long-term obligations.

A solvent business has sufficient assets to cover liabilities over the long term.

Lenders and investors often evaluate solvency before providing financing.

Strong solvency generally indicates financial stability.

- Current Ratio

The current ratio measures short-term financial health.

Formula:

Current Assets ÷ Current Liabilities

Example:

Current Assets = $100,000

Current Liabilities = $50,000

Current Ratio = 2.0

A ratio above 1 generally indicates the business can meet short-term obligations.

- Quick Ratio

The quick ratio is a stricter measure of liquidity.

Formula:

(Current Assets – Inventory) ÷ Current Liabilities

Since inventory may not be easily converted into cash, the quick ratio provides a clearer view of immediate liquidity.

Lenders frequently review this ratio when evaluating loan applications.

- Debt-to-Equity Ratio

The debt-to-equity ratio compares total liabilities to owner’s equity.

Formula:

Total Liabilities ÷ Equity

Example:

Liabilities = $300,000

Equity = $150,000

Debt-to-Equity Ratio = 2.0

A higher ratio may indicate greater financial risk.

A lower ratio generally suggests a more conservative financial structure.

- Interest Expense

Interest expense is the cost of borrowing money.

Examples include interest paid on:

- Business loans

- Credit cards

- Equipment financing

- Commercial mortgages

Interest expense appears on the income statement and affects net income.

Reducing unnecessary debt can lower interest costs and improve profitability.

- Capital Expenditure (CapEx)

Capital expenditures are investments in long-term assets that provide value for multiple years.

Examples include:

- Buildings

- Equipment

- Vehicles

- Technology infrastructure

CapEx differs from regular operating expenses because the asset provides long-term benefits.

Business owners often budget carefully for capital expenditures due to their significant cost.

- Working Capital Ratio

The working capital ratio evaluates short-term financial strength.

Formula:

Current Assets ÷ Current Liabilities

A ratio between 1.2 and 2.0 is often considered healthy for many businesses.

This metric helps identify potential liquidity issues before they become serious problems.

- Retained Earnings

Retained earnings represent accumulated profits that remain in the business after dividends or owner distributions.

Businesses often use retained earnings to:

- Expand operations

- Purchase equipment

- Hire employees

- Fund growth initiatives

Growing retained earnings often indicate long-term business success.

- Owner’s Draw

An owner’s draw occurs when a business owner withdraws money from the company for personal use.

Common in:

- Sole proprietorships

- Partnerships

- Some LLCs

Owner’s draws are not considered business expenses.

They reduce owner’s equity rather than affecting profit.

- Dividend

A dividend is a distribution of profits to shareholders.

Corporations may pay dividends:

- Quarterly

- Semi-annually

- Annually

Dividends reward investors but reduce retained earnings.

Not all businesses distribute dividends, especially those focused on growth.

- Payroll

Payroll refers to the process of paying employees and managing related obligations.

Payroll includes:

- Wages

- Salaries

- Bonuses

- Payroll taxes

- Employee benefits

Accurate payroll processing is essential for legal compliance and employee satisfaction.

- Payroll Taxes

Payroll taxes are taxes employers withhold or pay on behalf of employees.

Examples include:

- Social Security taxes

- Medicare taxes

- Federal unemployment taxes

- State payroll taxes

Failure to properly manage payroll taxes can result in significant penalties.

- Sales Tax

Sales tax is collected from customers on taxable goods and services.

Businesses act as tax collectors by:

- Charging sales tax.

- Collecting it from customers.

- Remitting it to the appropriate tax authority.

Sales tax requirements vary by state and locality throughout the United States.

- Tax Deduction

A tax deduction reduces taxable income.

Common business deductions include:

- Office expenses

- Advertising costs

- Business travel

- Software subscriptions

- Professional services

- Vehicle expenses

Proper documentation is essential to support deductions during an audit.

- Audit

An audit is an examination of financial records and statements.

Audits may be performed by:

- Internal auditors

- Independent accounting firms

- Government agencies

The purpose is to verify financial accuracy and compliance with applicable standards.

Well-organized records make audits significantly easier.

- Audit Trail

An audit trail is a chronological record of all financial transactions and accounting activities within a business.

An audit trail shows:

- Who made a transaction

- When it occurred

- What was changed

- Why the change was made

Modern accounting software automatically creates audit trails, helping businesses maintain transparency and accountability.

Audit trails are particularly valuable during tax audits, fraud investigations, and financial reviews.

- Internal Controls

Internal controls are policies and procedures designed to protect business assets and ensure accurate financial reporting.

Examples include:

- Separation of duties

- Approval requirements

- Password protection

- Inventory counts

- Bank reconciliations

Strong internal controls help prevent:

- Fraud

- Theft

- Accounting errors

- Financial mismanagement

Even small businesses benefit from implementing basic internal controls.

- GAAP (Generally Accepted Accounting Principles)

GAAP refers to a standardized set of accounting rules and guidelines used in the United States.

These principles ensure:

- Consistency

- Accuracy

- Transparency

- Comparability

Many lenders, investors, and government agencies expect financial statements to comply with GAAP standards.

Understanding GAAP helps business owners interpret financial reports more effectively.

- Financial Statements

Financial statements are formal reports that summarize a company’s financial activities.

The three primary financial statements include:

Balance Sheet

Shows assets, liabilities, and equity.

Income Statement

Shows revenue, expenses, and profit.

Cash Flow Statement

Shows cash inflows and outflows.

Together, these reports provide a complete picture of financial performance and position.

- Revenue Recognition

Revenue recognition refers to determining when revenue should be recorded.

Under accrual accounting, revenue is recognized when earned rather than when payment is received.

Proper revenue recognition ensures:

- Accurate reporting

- Regulatory compliance

- Reliable financial statements

Businesses with contracts, subscriptions, or long-term projects must pay particular attention to revenue recognition rules.

- Bad Debt Expense

Bad debt expense represents money a business expects will never be collected from customers.

For example:

If a customer files bankruptcy and cannot pay an invoice, the amount may be recorded as bad debt.

Monitoring bad debt helps businesses evaluate customer credit policies and collection procedures.

- Allowance for Doubtful Accounts

This account estimates future uncollectible receivables.

Rather than waiting until a customer fails to pay, businesses estimate potential losses in advance.

Benefits include:

- More accurate financial statements

- Improved forecasting

- Better risk management

This accounting practice is commonly used in accrual accounting systems.

- Inventory Turnover

Inventory turnover measures how efficiently inventory is sold and replaced.

Formula:

Cost of Goods Sold ÷ Average Inventory

A higher turnover ratio often indicates:

- Strong sales

- Efficient inventory management

A lower ratio may suggest:

- Overstocking

- Obsolete inventory

- Weak demand

Inventory turnover is especially important for retailers and manufacturers.

- Accounts Receivable Aging

Accounts receivable aging categorizes unpaid invoices based on how long they have been outstanding.

Typical categories include:

- Current

- 1–30 days overdue

- 31–60 days overdue

- 61–90 days overdue

- Over 90 days overdue

This report helps business owners identify collection issues and improve cash flow management.

- Markup

Markup is the amount added to the cost of a product to determine its selling price.

Formula:

(Selling Price – Cost) ÷ Cost × 100

Example:

Cost = $50

Selling Price = $75

Markup = 50%

Understanding markup helps businesses establish profitable pricing strategies.

- Return on Investment (ROI)

ROI measures the profitability of an investment.

Formula:

(Net Profit ÷ Investment Cost) × 100

Example:

Investment = $10,000

Profit Generated = $2,500

ROI = 25%

Business owners frequently use ROI when evaluating:

- Marketing campaigns

- Equipment purchases

- New business initiatives

- Return on Assets (ROA)

ROA measures how efficiently a company uses its assets to generate profit.

Formula:

Net Income ÷ Total Assets

A higher ROA generally indicates better asset utilization and stronger operational efficiency.

Investors often review this ratio when comparing businesses.

- Return on Equity (ROE)

ROE measures profitability relative to shareholders’ equity.

Formula:

Net Income ÷ Equity

ROE helps business owners and investors evaluate how effectively capital is being used to generate returns.

A consistently strong ROE often signals a healthy business.

- Gross Receipts

Gross receipts represent the total amount of money received by a business before any deductions.

Gross receipts may include:

- Product sales

- Service revenue

- Interest income

- Rental income

Gross receipts differ from profit because expenses have not yet been deducted.

Many tax filings require reporting gross receipts.

- Business Credit

Business credit reflects a company’s borrowing history and creditworthiness.

Strong business credit can help companies:

- Obtain loans

- Secure vendor financing

- Negotiate better interest rates

- Increase purchasing power

Building business credit is an important part of long-term financial management.

- Line of Credit

A line of credit is a flexible financing arrangement that allows businesses to borrow funds as needed.

Unlike traditional loans:

- Businesses borrow only what they need.

- Interest is charged only on amounts used.

Lines of credit are often used to manage short-term cash flow fluctuations.

- Equity Financing

Equity financing involves raising money by selling ownership interests in a company.

Sources may include:

- Angel investors

- Venture capital firms

- Private investors

Advantages:

- No loan repayment requirements

Disadvantages:

- Ownership dilution

Business owners should carefully evaluate the trade-offs before pursuing equity financing.

- Debt Financing

Debt financing involves borrowing money that must be repaid with interest.

Examples include:

- Business loans

- SBA loans

- Equipment financing

- Commercial mortgages

Debt financing allows owners to retain control of the company but creates repayment obligations.

- Cash Reserve

A cash reserve is money set aside for emergencies or future opportunities.

Strong cash reserves help businesses:

- Manage economic downturns

- Cover unexpected expenses

- Handle seasonal fluctuations

- Invest in growth opportunities

Financial experts often recommend maintaining several months of operating expenses in reserve.

- Burn Rate

Burn rate measures how quickly a company spends cash.

It is especially important for:

- Startups

- Growth-stage companies

- Venture-backed businesses

Example:

If a company spends $50,000 per month more than it earns, its monthly burn rate is $50,000.

Monitoring burn rate helps prevent cash shortages.

- Runway

Runway estimates how long a business can continue operating before running out of cash.

Formula:

Cash Available ÷ Monthly Burn Rate

Example:

Cash Reserve = $300,000

Monthly Burn Rate = $25,000

Runway = 12 Months

Understanding runway helps business owners plan fundraising and cost-management strategies.

- Financial KPI (Key Performance Indicator)

Financial KPIs are measurable metrics used to evaluate business performance.

Common accounting-related KPIs include:

- Revenue growth

- Gross margin

- Net profit margin

- Cash flow

- Current ratio

- Accounts receivable turnover

Tracking KPIs regularly helps identify strengths and weaknesses before they become major issues.

- Budget Variance

Budget variance measures the difference between planned and actual results.

Example:

Budgeted Marketing Expense: $5,000

Actual Marketing Expense: $6,500

Variance: $1,500 unfavorable

Analyzing variances helps businesses improve planning accuracy and financial discipline.

- Financial Health

Financial health refers to the overall strength and stability of a business.

Key indicators include:

- Profitability

- Liquidity

- Solvency

- Cash flow

- Growth trends

Business owners who understand accounting terminology are better equipped to evaluate financial health and make informed decisions.

Conclusion

Accounting is often viewed as a complex subject reserved for accountants and finance professionals. However, every business owner can benefit significantly from understanding fundamental accounting terminology.

Whether you’re reviewing financial statements, applying for a loan, preparing taxes, managing cash flow, or evaluating growth opportunities, accounting knowledge provides a strong foundation for smarter decision-making.

The terms covered in this guide—from assets and liabilities to cash flow, profitability ratios, financial statements, and business financing concepts—represent the core language of business finance.