Accounting is often called the language of business, and debit and credit are its foundation. Whether you are a small business owner, accounting student, entrepreneur, bookkeeper, or finance professional, understanding debit and credit rules is essential for maintaining accurate financial records.

Many beginners believe that debits always mean “good” and credits always mean “bad,” or that debits increase money while credits decrease money. In reality, accounting is much more systematic. Debits and credits are simply a method used to record financial transactions and ensure that the accounting equation remains balanced.

Every financial transaction affects at least two accounts. This concept is known as double-entry bookkeeping, a system that has been used for centuries and remains the backbone of modern accounting. When one account is debited, another account must be credited by the same amount.

This comprehensive guide explains debit and credit rules in simple language, provides practical examples, and demonstrates how businesses use these principles every day.

What Are Debits and Credits?

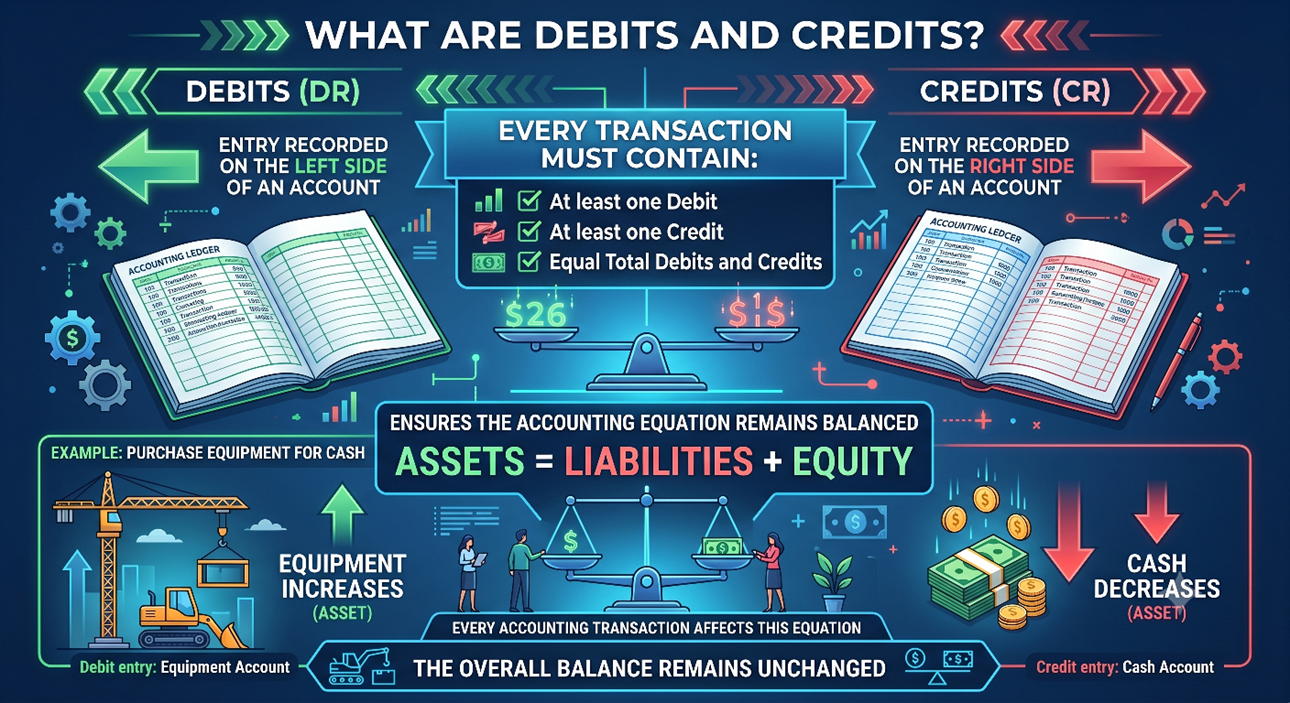

Debits and credits are accounting entries used to record transactions.

A debit (DR) is an entry recorded on the left side of an account.

A credit (CR) is an entry recorded on the right side of an account.

Every transaction must contain:

- At least one debit

- At least one credit

- Equal total debits and credits

This ensures the accounting equation remains balanced.

Assets = Liabilities + Equity

Every accounting transaction affects this equation.

For example:

If a business purchases equipment for cash:

- Equipment increases

- Cash decreases

The overall balance remains unchanged.

Understanding Double-Entry Bookkeeping

Double-entry bookkeeping requires every transaction to affect at least two accounts.

For example:

A company purchases office furniture for $5,000 cash.

Journal Entry:

Debit: Furniture $5,000

Credit: Cash $5,000

The business now owns more furniture and has less cash.

The books remain balanced because:

Total Debits = Total Credits = $5,000

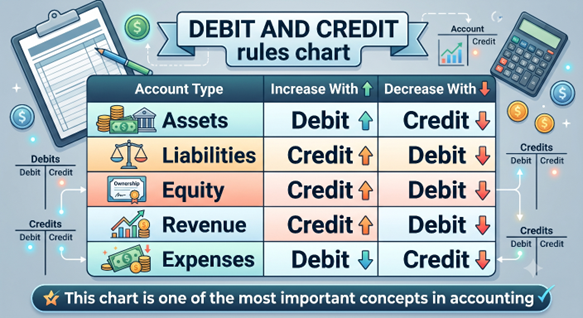

Modern Accounting Classification

Modern accounting focuses on five major account types:

- Assets

- Liabilities

- Equity

- Revenue

- Expenses

Understanding these categories makes debit and credit rules much easier.

Debit and Credit Rules Chart

Understanding Assets

Assets are resources owned by a business.

Examples:

- Cash

- Equipment

- Inventory

- Accounts Receivable

- Buildings

- Vehicles

Increase = Debit

Decrease = Credit

Business receives $5,000 cash.

Debit Cash $5,000

Cash increases, so debit is used.

Understanding Liabilities

Liabilities are obligations owed to others.

Examples:

- Loans

- Accounts Payable

- Notes Payable

- Credit Card Debt

Increase = Credit

Decrease = Debit

Business obtains a bank loan of $20,000.

Debit Cash $20,000

Credit Loan Payable $20,000

Understanding Equity

Equity represents the owner’s interest in the business.

Examples:

- Owner’s Capital

- Common Stock

- Retained Earnings

Increase = Credit

Decrease = Debit

Owner invests $15,000.

Debit Cash $15,000

Credit Owner’s Equity $15,000

Understanding Revenue

Revenue is income earned from business operations.

Examples:

- Sales Revenue

- Service Revenue

- Consulting Revenue

Increase = Credit

Decrease = Debit

Company earns $3,000 from consulting services.

Debit Cash $3,000

Credit Service Revenue $3,000

Understanding Expenses

Expenses are costs incurred to generate revenue.

Examples:

- Rent

- Utilities

- Salaries

- Insurance

- Advertising

Increase = Debit

Decrease = Credit

Pay utility bill of $400.

Debit Utilities Expense $400

Credit Cash $400

The Accounting Equation and Debits and Credits

The accounting equation is:

Assets = Liabilities + Equity

Every transaction must maintain this balance.

Example:

Owner invests $50,000.

Assets increase by $50,000.

Equity increases by $50,000.

Equation remains balanced.

Common Debit and Credit Examples

Example 1: Cash Sale

A store sells goods for $1,000 cash.

Debit Cash $1,000

Credit Sales Revenue $1,000

Example 2: Purchase Equipment with Cash

Equipment purchased for $5,000.

Debit Equipment $5,000

Credit Cash $5,000

Example 3: Purchase Inventory on Credit

Inventory purchased for $8,000.

Debit Inventory $8,000

Credit Accounts Payable $8,000

Example 4: Pay Vendor

Business pays supplier $2,000.

Debit Accounts Payable $2,000

Credit Cash $2,000

Example 5: Receive Customer Payment

Customer pays outstanding invoice of $1,500.

Debit Cash $1,500

Credit Accounts Receivable $1,500

Journal Entries Explained

Journal entries are the formal recording of transactions.

Every journal entry includes:

- Date

- Accounts affected

- Debit amount

- Credit amount

- Description

Example:

Date: July 1

Debit Rent Expense $1,200

Credit Cash $1,200

Description: Monthly office rent payment.

T-Accounts and Debit Credit Rules

A T-account visually represents transactions.

Example Cash Account:

Debit Side | Credit Side

$10,000 | $2,000

$5,000 |

Balance = $13,000

The left side records debits.

The right side records credits.

Accounts Receivable Example

Company sells products on credit for $5,000.

Debit Accounts Receivable $5,000

Credit Sales Revenue $5,000

When customer pays:

Debit Cash $5,000

Credit Accounts Receivable $5,000

Accounts Payable Example

Company purchases supplies on credit for $2,000.

Debit Supplies $2,000

Credit Accounts Payable $2,000

When payment is made:

Debit Accounts Payable $2,000

Credit Cash $2,000

Payroll Example

Employees earn wages of $4,000.

Debit Salaries Expense $4,000

Credit Cash $4,000

Or

Credit Salaries Payable $4,000 if unpaid.

Loan Transaction Example

Company receives loan proceeds of $100,000.

Debit Cash $100,000

Credit Loan Payable $100,000

Loan liability increases.

Depreciation Example

Equipment depreciation expense is $500.

Debit Depreciation Expense $500

Credit Accumulated Depreciation $500

Dividend Example

Company pays shareholders $2,000.

Debit Dividends $2,000

Credit Cash $2,000

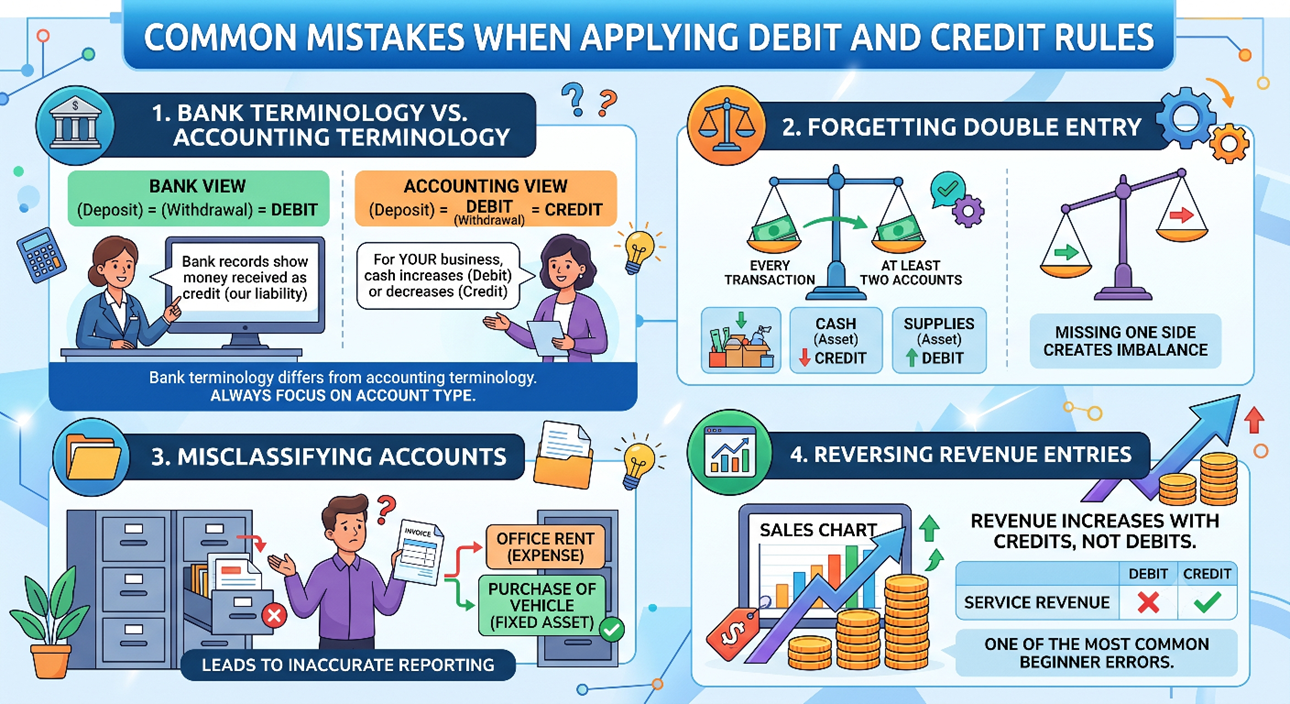

Common Mistakes When Applying Debit and Credit Rules

One of the most common mistakes beginners make when learning accounting is confusing banking terminology with accounting terminology. Many people assume that a bank deposit should always be recorded as a credit and a bank withdrawal should always be recorded as a debit. This misunderstanding occurs because banks view transactions from their perspective rather than the customer’s perspective. In accounting, whether an entry is a debit or a credit depends entirely on the type of account being affected. Instead of relying on banking terminology, it is important to identify the account category—such as asset, liability, equity, revenue, or expense—and then apply the appropriate debit and credit rules.

Another frequent error is forgetting the principle of double-entry bookkeeping. Every financial transaction must affect at least two accounts, with the total debits always equaling the total credits. Beginners sometimes record only one side of a transaction, which causes the accounting records to become unbalanced. For example, if a business pays rent and records only the Rent Expense account without reducing Cash, the books will no longer accurately reflect the company’s financial position. Understanding that every transaction has both a debit and a credit side is essential for maintaining accurate financial records.

Misclassifying accounts is another mistake that can create significant reporting problems. New accountants and business owners sometimes record expenses as assets or classify liabilities incorrectly. For instance, treating a monthly utility bill as an asset instead of an expense can overstate the company’s resources and distort profitability. Proper account classification ensures that financial statements accurately represent the business’s financial health and provide reliable information for decision-making.

Reversing revenue entries is also a common beginner error. Revenue accounts increase with credits, not debits. Because many people associate credits with reductions, they may mistakenly debit a revenue account when recording a sale. Doing so can understate income and lead to inaccurate financial statements. For example, when a company earns revenue from providing services, the correct entry is to debit Cash or Accounts Receivable and credit Service Revenue. Remembering that revenue increases with credits can help avoid one of the most frequent mistakes in accounting.

Easy Memory Trick for Debits and Credits

Remember:

D = Dividends

E = Expenses

A = Assets

These increase with Debits.

L = Liabilities

E = Equity

R = Revenue

These increase with Credits.

Many accounting students use this formula to remember the rules.

How Accounting Software Handles Debits and Credits

Modern accounting software automates journal entries.

Popular software includes:

- QuickBooks

- Xero

- FreshBooks

- Sage 50

Although software automates entries, understanding the underlying debit and credit rules remains important.

Real-World Business Scenario

Imagine a small marketing agency:

- Owner invests $25,000

- Purchases equipment for $5,000

- Earns $10,000 from clients

- Pays rent of $1,500

- Pays employee salaries of $3,000

Each transaction requires corresponding debit and credit entries.

These entries collectively produce accurate financial statements.

Best Practices for Learning Debits and Credits

- Memorize the account categories.

- Practice journal entries daily.

- Use T-accounts.

- Understand the accounting equation.

- Review real business transactions.

- Learn the reasoning behind entries rather than memorizing them.

Consistent practice is the fastest way to master accounting fundamentals.

Conclusion

Debits and credits form the foundation of accounting and bookkeeping. While the rules may seem confusing at first, they become much easier when you understand how different account types behave. Assets and expenses increase with debits, while liabilities, equity, and revenue increase with credits.

Every transaction recorded by a business follows the principle of double-entry bookkeeping, ensuring that total debits always equal total credits. This system helps maintain accurate financial records, supports reliable financial reporting, and provides business owners with the information needed to make informed decisions.

Whether you are a student learning accounting, an entrepreneur managing finances, or a professional working in bookkeeping, mastering debit and credit rules is one of the most valuable skills you can develop. By understanding the accounting equation, practicing journal entries, and applying the debit and credit framework consistently, you can build a strong foundation for success in accounting and financial management.