Accurate financial records are the foundation of every successful business. Whether you run a small startup, a growing company, or a large corporation, maintaining organized accounting records is essential for making informed business decisions and complying with financial reporting requirements. One of the most important tools used in the accounting process is the Trial Balance.

A trial balance serves as a checkpoint in the accounting cycle. It helps businesses verify that total debits equal total credits after recording financial transactions. Before preparing financial statements such as the income statement and balance sheet, accountants use the trial balance to identify errors and confirm the accuracy of ledger balances.

In the United States, businesses of all sizes rely on trial balances to maintain financial accuracy, support audits, and ensure compliance with accounting standards. Although modern accounting software automates much of the process, understanding how a trial balance works remains essential for accountants, bookkeepers, business owners, and finance professionals.

This comprehensive guide explains everything you need to know about trial balances, including their purpose, importance, preparation process, examples, advantages, limitations, and best practices.

What Is a Trial Balance?

A trial balance is an accounting report that lists all general ledger account balances at a specific point in time. It displays the debit balances in one column and credit balances in another.

The primary purpose of a trial balance is to verify that the total debits equal the total credits recorded in the accounting system.

According to the double-entry accounting system, every financial transaction affects at least two accounts. One account receives a debit entry, while another receives a corresponding credit entry. Because total debits should always equal total credits, the trial balance acts as a tool to check whether the books are mathematically balanced.

A trial balance is typically prepared at the end of an accounting period, such as monthly, quarterly, or annually, before creating financial statements.

Why Is a Trial Balance Important?

A trial balance plays a critical role in the accounting process. It serves as an internal control mechanism that helps ensure accounting records are accurate and complete.

Key reasons why trial balances are important include:

Error Detection

The trial balance helps identify bookkeeping mistakes. If total debits do not equal total credits, an error exists somewhere in the accounting records.

Financial Statement Preparation

Accountants use trial balances as the foundation for preparing financial statements.

Audit Support

External and internal auditors often review trial balances when examining a company’s financial records.

Compliance

Accurate accounting records help businesses comply with financial reporting regulations and tax requirements.

Objectives of Preparing a Trial Balance

The trial balance serves several important objectives within the accounting cycle.

Verify Arithmetic Accuracy

One of the primary objectives of a trial balance is to confirm the mathematical accuracy of accounting records. Under the double-entry accounting system, every transaction affects at least two accounts, with total debits always equal to total credits. When a trial balance is prepared, the total of the debit column should match the total of the credit column. If the totals do not agree, it indicates that an error has occurred in recording, posting, or calculating transactions. This verification helps accountants identify discrepancies before moving to the next stage of financial reporting.

Summarize Ledger Accounts

A trial balance provides a summarized view of all account balances from the general ledger in a single report. Instead of reviewing individual ledger accounts separately, accountants can quickly see the balances of assets, liabilities, equity, revenues, and expenses in one place. This consolidated summary makes it easier to analyze the financial data of a business and serves as a useful reference for management, auditors, and accounting professionals.

Facilitate Financial Reporting

The trial balance acts as the foundation for preparing financial statements such as the income statement, balance sheet, and cash flow statement. Since it contains the ending balances of all ledger accounts, accountants use it to organize and transfer financial information into the appropriate statements. An accurate trial balance helps ensure that financial reports are prepared correctly and reflect the true financial position and performance of the business.

Identify Errors

Another important objective of a trial balance is to help detect certain types of accounting errors. For example, it can reveal mistakes such as unequal debit and credit entries, incorrect postings, mathematical calculation errors, or incomplete transaction recordings. While a trial balance cannot detect every accounting error, it serves as an effective tool for identifying issues that cause debit and credit totals to be unequal. Detecting these errors early helps prevent inaccurate financial reporting.

Support Internal Controls

A trial balance contributes to strong internal controls by promoting accuracy, accountability, and financial discipline within an organization. Regular preparation and review of trial balances help ensure that accounting records are maintained properly and that financial transactions are recorded consistently. It also provides management with a mechanism to monitor the integrity of financial data, reduce the risk of errors and fraud, and improve overall financial governance.

Understanding the Double-Entry Accounting System

To understand a trial balance, it is essential to understand double-entry accounting.

Every transaction affects at least two accounts.

For example:

A company purchases office supplies for $500 cash.

| Account | Debit | Credit |

| Office Supplies Expense | $500 | |

| Cash | $500 |

The debit increases expenses, while the credit decreases cash.

Since every transaction contains equal debits and credits, the accounting equation remains balanced.

This principle forms the basis of the trial balance.

Components of a Trial Balance

A typical trial balance contains the following elements:

Company Name – Identifies the business preparing the report.

Report Title – Indicates that the document is a trial balance.

Reporting Date – Shows the specific date for which balances are presented.

Account Names – Lists all general ledger accounts.

Debit Column – Displays accounts with debit balances.

Credit Column – Displays accounts with credit balances.

Total Balances – Shows the sum of debit balances and credit balances.

Format of a Trial Balance

A standard trial balance generally appears as follows:

| Account Name | Debit ($) | Credit ($) |

| Cash | 25,000 | |

| Accounts Receivable | 10,000 | |

| Equipment | 15,000 | |

| Accounts Payable | 8,000 | |

| Revenue | 30,000 | |

| Capital | 12,000 | |

| Expenses | 20,000 | |

| Total | 70,000 | 70,000 |

The total debits and credits must match.

Types of Trial Balance

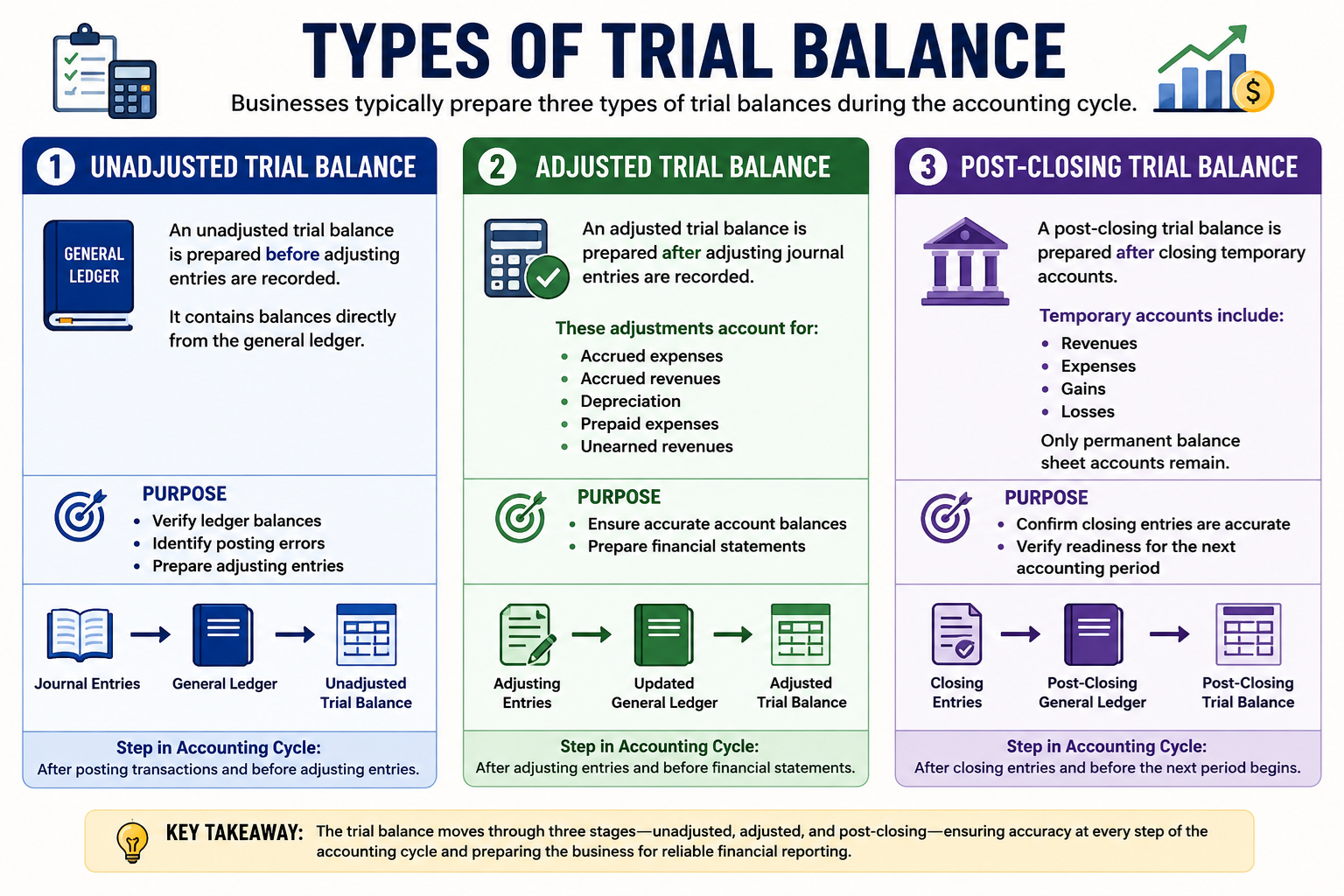

Businesses typically prepare three types of trial balances during the accounting cycle.

Unadjusted Trial Balance

An unadjusted trial balance is prepared before adjusting entries are recorded.

It contains balances directly from the general ledger.

Purpose

- Verify ledger balances

- Identify posting errors

- Prepare adjusting entries

Adjusted Trial Balance

An adjusted trial balance is prepared after adjusting journal entries are recorded.

These adjustments account for:

- Accrued expenses

- Accrued revenues

- Depreciation

- Prepaid expenses

- Unearned revenues

Purpose

- Ensure accurate account balances

- Prepare financial statements

Post-Closing Trial Balance

A post-closing trial balance is prepared after closing temporary accounts.

Temporary accounts include:

- Revenues

- Expenses

- Gains

- Losses

Only permanent balance sheet accounts remain.

Purpose

- Confirm closing entries are accurate

- Verify readiness for the next accounting period

How to Prepare a Trial Balance

Preparing a trial balance involves several steps.

Step 1: Record Transactions

Record all financial transactions in journal entries.

Example:

Sale of goods worth $5,000 on credit.

| Account | Debit | Credit |

| Accounts Receivable | $5,000 | |

| Sales Revenue | $5,000 |

Step 2: Post Entries to Ledger Accounts

Transfer journal entries into the general ledger.

Step 3: Calculate Account Balances

Determine ending balances for all ledger accounts.

Step 4: List Account Balances

Enter each account and balance into the trial balance.

Step 5: Separate Debits and Credits

Place debit balances in the debit column and credit balances in the credit column.

Step 6: Calculate Totals

Add all debit balances and all credit balances.

Step 7: Compare Totals

If totals match, the trial balance is considered balanced.

Trial Balance Example

Consider the following account balances for ABC Company.

| Account | Debit ($) | Credit ($) |

| Cash | 40,000 | |

| Accounts Receivable | 15,000 | |

| Inventory | 20,000 | |

| Equipment | 50,000 | |

| Accounts Payable | 18,000 | |

| Bank Loan | 25,000 | |

| Owner’s Capital | 40,000 | |

| Sales Revenue | 55,000 | |

| Rent Expense | 5,000 | |

| Salaries Expense | 8,000 | |

| Utilities Expense | 500 | |

| Total | 138,500 | 138,500 |

Because the totals are equal, the trial balance balances successfully.

Relationship Between Trial Balance and Financial Statements

The trial balance serves as the bridge between accounting records and financial statements.

Income Statement

Prepared using:

- Revenue accounts

- Expense accounts

Balance Sheet

Prepared using:

- Assets

- Liabilities

- Equity

Cash Flow Statement

Uses information derived from financial statements and account balances.

Without an accurate trial balance, financial statements may contain errors.

Common Errors Detected by a Trial Balance

A trial balance can reveal several types of accounting mistakes.

Unequal Posting

Unequal posting occurs when a transaction is recorded with a debit entry but the corresponding credit entry is either missing or recorded for a different amount. Since the double-entry accounting system requires every debit to have an equal credit, such mistakes cause an imbalance in the accounting records. For example, if a company purchases equipment for $5,000 and records a debit of $5,000 to the Equipment account but mistakenly records only a $4,000 credit to Cash, the trial balance totals will not match. This discrepancy alerts accountants that an error exists and needs investigation.

Calculation Errors

Calculation errors are mathematical mistakes made while determining account balances or totaling the debit and credit columns. These errors can occur when adding transactions within a ledger account, carrying forward balances incorrectly, or totaling the trial balance itself. For instance, if the actual balance of an expense account should be $8,500 but is mistakenly calculated as $8,050, the trial balance may become unbalanced. Identifying and correcting these arithmetic mistakes is one of the key functions of the trial balance.

Posting Errors

Posting errors occur when journal entries are transferred incorrectly to the general ledger. One common example is posting an amount to the wrong side of an account. For instance, an expense account that should receive a debit entry may accidentally be credited instead. Such mistakes affect the normal balance of accounts and often result in unequal debit and credit totals. A trial balance can help uncover these errors because the resulting account balances may cause the overall totals to differ.

Omitted Entries

An omitted entry occurs when one side of a transaction is not recorded in the accounting system. For example, a company may correctly debit Accounts Receivable for a credit sale but forget to credit Sales Revenue. Because only one side of the transaction has been entered, the accounting equation becomes unbalanced. When the trial balance is prepared, the debit and credit totals will not agree, indicating that a transaction may be incomplete. Detecting omitted entries helps ensure that all financial transactions are fully recorded.

Errors Not Detected by a Trial Balance

A balanced trial balance does not guarantee complete accuracy. Certain mistakes remain hidden.

1. Error of Omission

An error of omission occurs when an entire transaction is completely left out of the accounting records. Since neither the debit side nor the credit side of the transaction is recorded, the trial balance will still balance.

Example:

A company purchases office supplies worth $1,000 on credit.

Correct entry:

| Account | Debit | Credit |

| Office Supplies Expense | $1,000 | |

| Accounts Payable | $1,000 |

If the accountant forgets to record this transaction entirely, both the debit and credit entries are missing. As a result, the trial balance remains balanced even though the accounting records are incomplete.

Why the trial balance cannot detect it:

Since both sides of the transaction are omitted, the debit and credit totals remain equal.

2. Error of Principle

An error of principle occurs when a transaction is recorded in violation of accounting principles, usually by classifying it under the wrong type of account. Although the transaction is recorded with equal debits and credits, the classification is incorrect.

Example:

A company purchases machinery for $20,000.

The machinery should be recorded as an asset:

| Account | Debit | Credit |

| Machinery | $20,000 | |

| Cash | $20,000 |

Instead, the accountant records it as a repair expense:

| Account | Debit | Credit |

| Repairs Expense | $20,000 | |

| Cash | $20,000 |

The debit and credit amounts are equal, so the trial balance balances. However, the machinery has been incorrectly classified as an expense rather than an asset.

Why the trial balance cannot detect it:

The transaction follows the double-entry system correctly, even though the account classification is wrong.

3. Compensating Errors

Compensating errors occur when two or more independent errors offset each other. The effect of one mistake is cancelled out by another, allowing the trial balance to remain balanced.

Example:

- Sales Revenue is understated by $500.

- Rent Expense is also understated by $500.

The two errors offset each other, and the debit and credit totals still match.

Why the trial balance cannot detect it:

The net effect of the errors is zero, so the equality between debits and credits is maintained.

4. Error of Original Entry

An error of original entry occurs when the wrong amount is recorded in the journal entry, but the incorrect amount is posted equally to both the debit and credit sides.

Example:

A business pays a utility bill of $850.

Correct entry:

| Account | Debit | Credit |

| Utilities Expense | $850 | |

| Cash | $850 |

However, the amount is mistakenly recorded as $580.

| Account | Debit | Credit |

| Utilities Expense | $580 | |

| Cash | $580 |

Both sides contain the same incorrect amount.

Why the trial balance cannot detect it:

Debits and credits remain equal despite the incorrect transaction value.

- Complete Reversal of Entries

A complete reversal occurs when the debit and credit sides of a transaction are accidentally switched. The correct accounts are used, but they are recorded on the wrong sides.

Example:

A customer pays $2,000 owed to the company.

Correct entry:

| Account | Debit | Credit |

| Cash | $2,000 | |

| Accounts Receivable | $2,000 |

Incorrect reversed entry:

| Account | Debit | Credit |

| Accounts Receivable | $2,000 | |

| Cash | $2,000 |

The transaction is recorded with equal debit and credit amounts, but the accounting treatment is completely reversed.

Trial Balance vs Balance Sheet

Many people confuse these two reports.

| Feature | Trial Balance | Balance Sheet |

| Purpose | Verify ledger balances | Show financial position |

| Accounts Included | All accounts | Assets, liabilities, equity |

| Internal/External | Internal report | External financial statement |

| Accounting Cycle Stage | Before financial statements | Final reporting stage |

Trial Balance vs General Ledger

| Feature | Trial Balance | General Ledger |

| Content | Summary balances | Detailed transactions |

| Purpose | Verify equality | Record transactions |

| Format | Report | Account records |

Conclusion

A trial balance is one of the most fundamental tools in accounting. It acts as a crucial checkpoint in the accounting cycle, ensuring that debit and credit entries remain balanced before financial statements are prepared. By summarizing ledger balances, identifying potential errors, supporting audits, and facilitating accurate reporting, the trial balance contributes significantly to financial integrity and business success.

For businesses across the United States, maintaining an accurate trial balance is not just an accounting best practice—it is an essential part of sound financial management. Whether prepared manually or generated through modern accounting software, a properly maintained trial balance helps organizations produce reliable financial statements, meet compliance requirements, and make better business decisions.